11/5 Weekly Report - Labor Market Alarm Bells Have Begun a Faint Ring..., Employment Data Deep Dive, Port Volumes, the Real Economic Realities + Ozone Live!

In this weekly Substack report - Don, Greg, and Joe tackle the latest concerning labor market data, look into the Apple Earnings report, tackle inflation issues, and provide a clear view of our Ports.

11/5 Substack MacroEdge Weekly Report

@DonMiami3, MacroEdge Chief Economist

@SquirtLagurtski, MacroEdge Contributor

@GregCrennan, MacroEdge Contributor

Labor Market Alarm Bells Have Begun a Faint Ring… Employment Data Deep Dive w/(@DonMiami3, Chief Economist)

Evening all -

Hope you’ve all had a great weekend. Want to keep this weekend's piece focused on the cooling labor market data that’s been rolling out over the last few weeks (and been something that we’ve been watching for nearly 2 quarters now). As expected - we are starting to see some sectors begin to contract at levels seen in previous recessions - notably in the logistics space, technology sector, in temporary help employees, and in the 16-19 unemployment rate.

If you haven’t yet joined our pre-access to the Insights Dashboard and O3 Weekly Reports - you can now at MacroEdge.net

While I am very wary of a slowing labor market now into the latter half of Q4 - I think holiday times and ‘seasonal grace’ may keep some sectors on the rails for now - such as the important elements in our Leading Employment Index basket like retail, travel and hospitality, and construction. It is still unlikely that we see shifts in these sectors until Q1 rolls around and companies take a step back and can closely analyze how they performed in their holiday seasons. While job cuts have been accelerating for the last 6 weeks now (as have initial and continuing claims) - recessions are not ‘race cars’ per se even though when one charts them on a graph they might look like it.

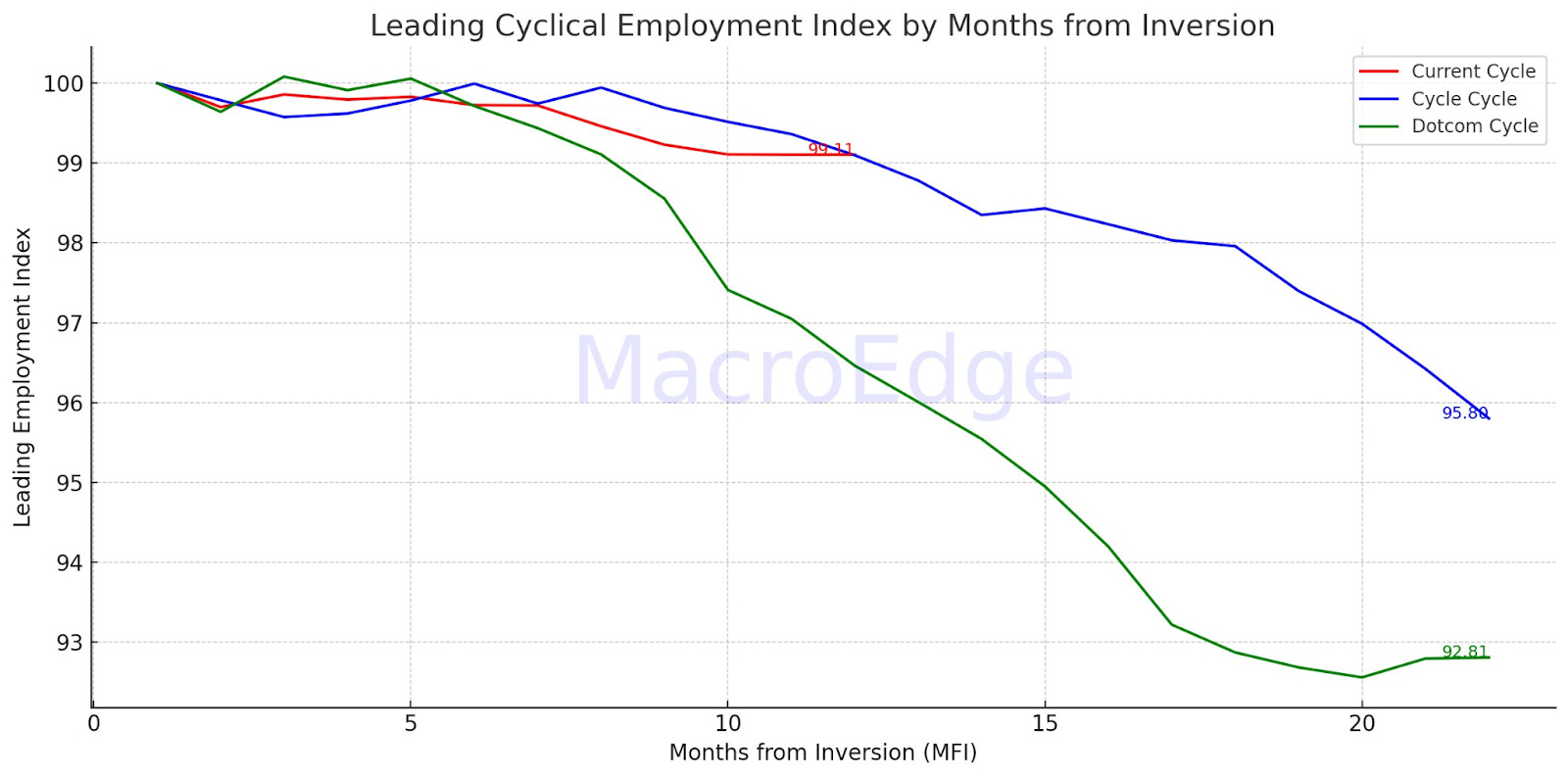

Our Leading Employment Index above provides us with an important idea about the depth of weakness seen among the most cyclical sectors of our labor market. In October (4) of the 7 in the basket expanded, and (3) contracted. Those seeing growth included temporary helps (holidays), retail, construction, and hospitality - while those seeing contraction include technology, HR employment, and manufacturing (which entered contraction for the first time this cycle). The next 3-5 months will give us a strong idea at where the larger employment market may be headed and our Employment Index still points to a recession based on historical measures from the past 50 years.

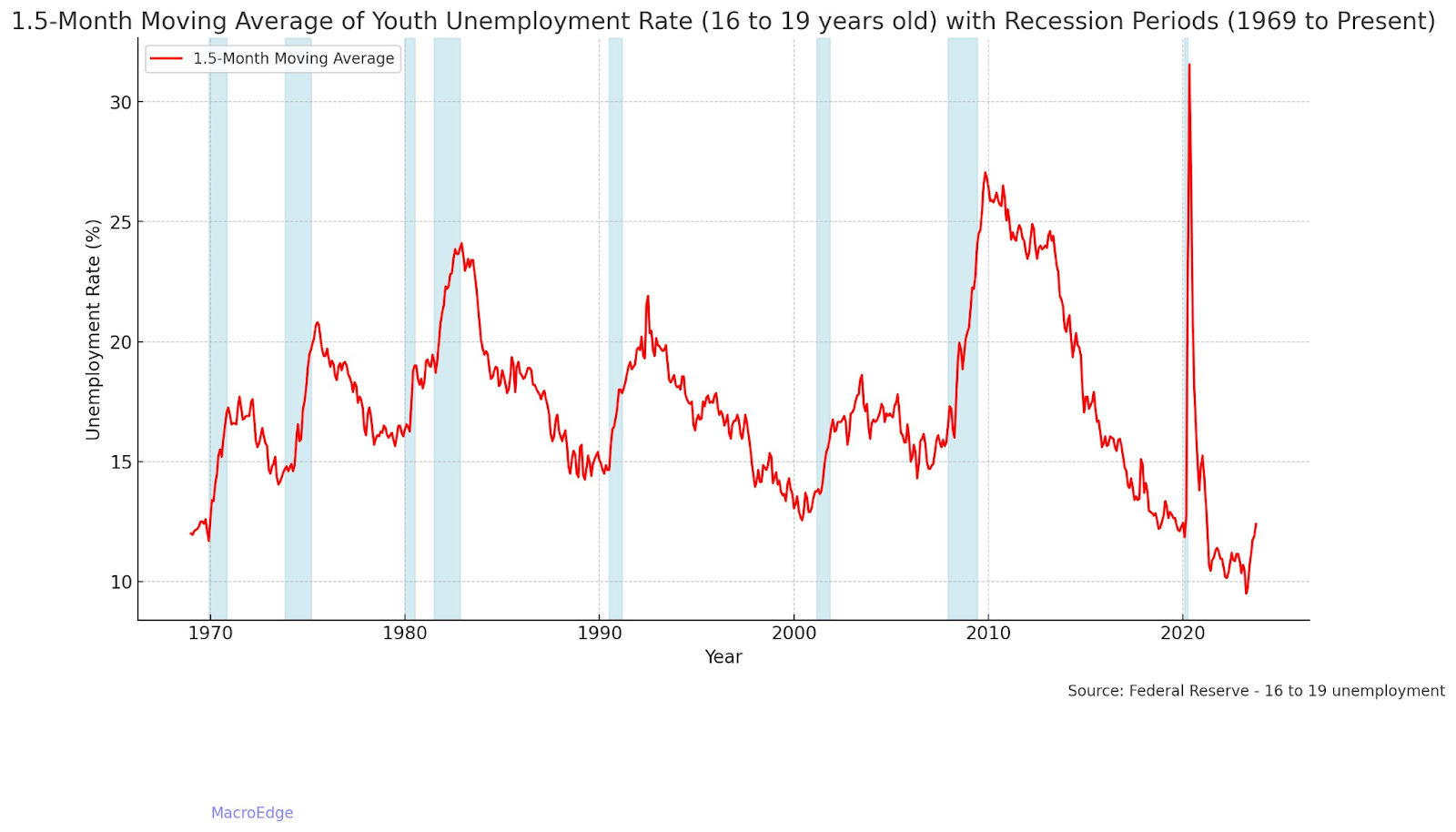

Looking at a smoothed line of the 16-19 unemployment rate, this gauge will be very important to watch going into early Q1 as it has been an important leading indicator in the past. As noted by Prof. Tamminga - 16 to 19-year-olds do make up a small but important % of discretionary spending in the United States (recessions happen at the margin).

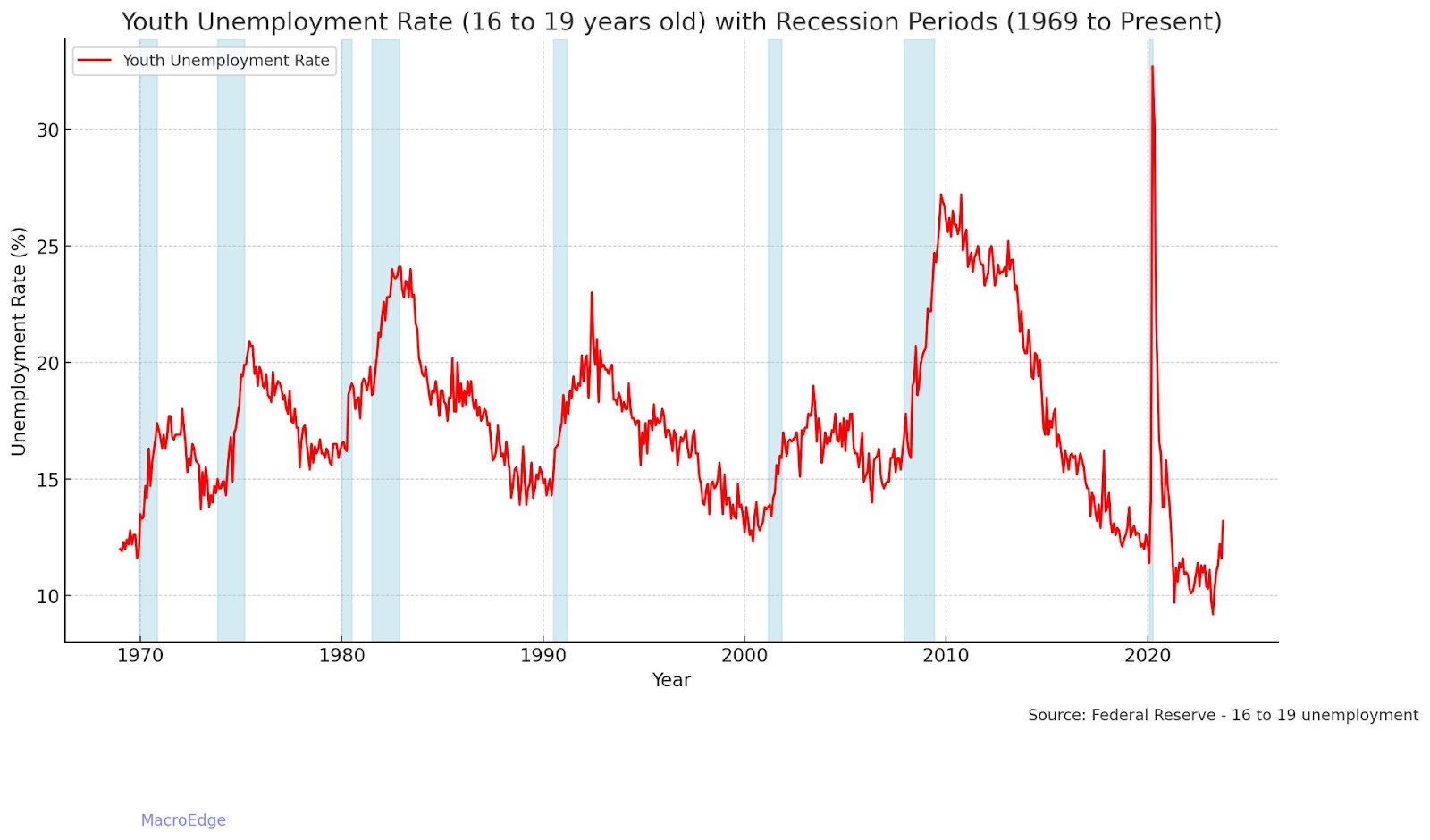

Here is the unsmoothed version:

Bloomberg’s Steve Hou even went ahead and edited our chart to give us all a better view without the COVID spike - calling it ‘revisionist truth’:

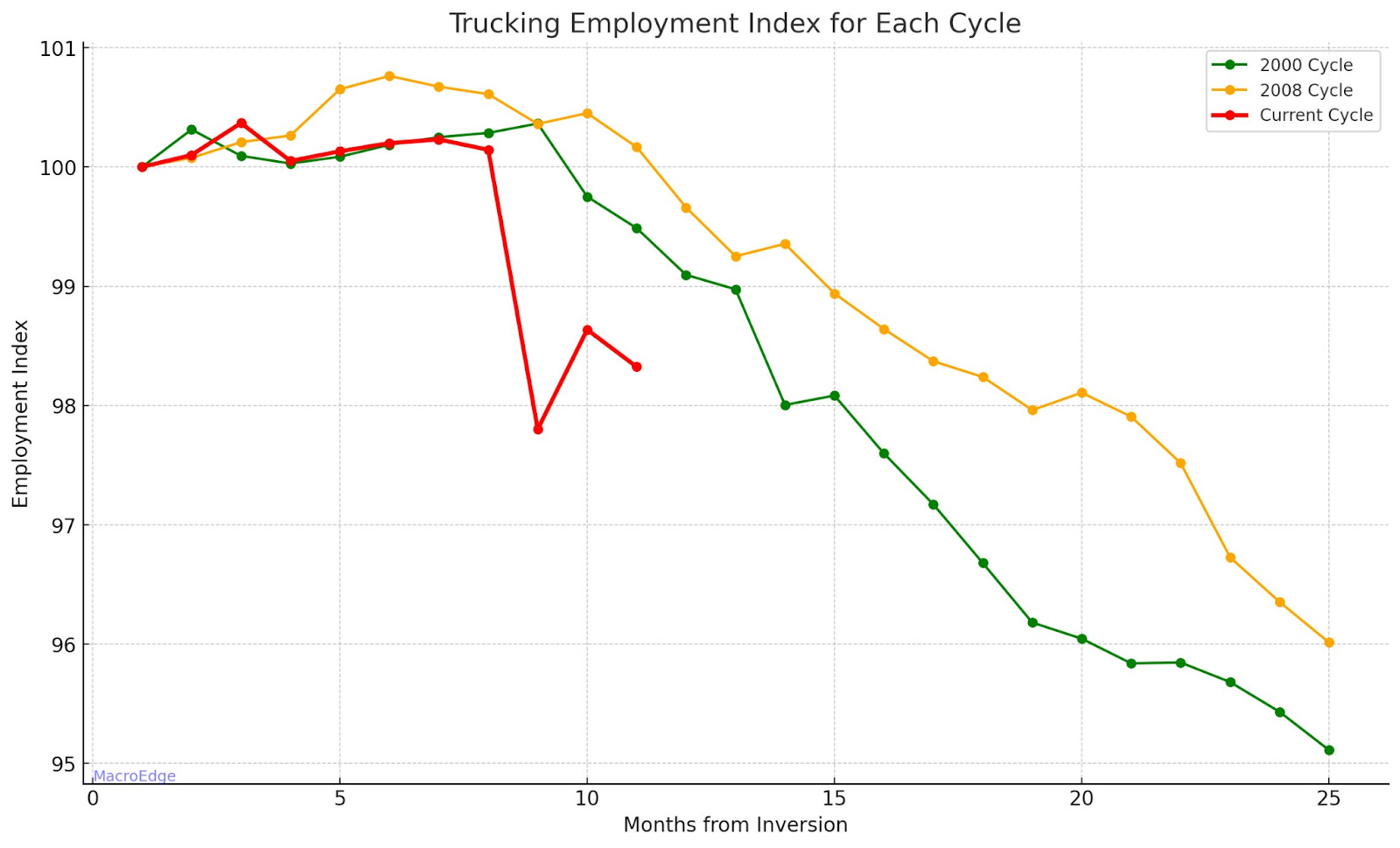

Trucking employment continues to warn us of the severe downturn happening in the transportation and logistics sectors. As noted by Craig of Freight Alley - the Citizens Bank of Iowa failure was actually caused by loan losses in the freight sector made by the bank. I noted on Twitter/X that this is the most significant trucking contraction this century underway in a space that went ballistic for the 2 years following the lockdown helicopter programs and QE(infinity).

We’re working on capturing a lot more data with some of our polls and research being conducted over the next month - and I look forward to sharing it with you all in the Ozone Portal as well as here every Sunday. I still anticipate based on our Leading Employment Index that the remainder of the quarter may be a bit of a lull period in terms of providing us with true direction on the next steps for the economy.

Have a great weekend and start to the week, rock on pals.

DJ

All Aboard (@SquirtLagurtski, MacoEdge Contributor)

In a September 2023 release the Port of Los Angeles reported an outlook for Q4 as positive but nothing to great either (not to worry all is well though), is that the case? The port volumes reported in the beginning of 2023 were down a staggering 31% YoY. SO where is that volume going? It turns we have been in what some call “inertia”, its fancy but what it boils down to is a combination of nearshoring, cost saving measures, and amplified by a large drop in Chinese imports over the last year. There’s been no greater worry of mine than the state of the logistics sector in the nation. On top of it all there’s a shift occurring in the polarity of the entire system, and its causing ripples through multiple adjacent sub sectors within an old and outdated system.

The southern ports, and eastern parts have largely benefitted from this process, Tennessee, Georgia, Virginia, New York, New Jersey have managed in some cases double their previously recorded volumes over the year to date, that’s where “inertia” comes into play and the source of a larger question, is that a feature of a long-term shift? Or will volumes reverse over time. The answer you should hear is “we don’t know”. Anyone else speculating otherwise is exposed to volatility that can be merciless to those not respecting a due diligence process. The last three years are being written off as if there just a product of Covid-19 and you shouldn’t expect destabilization of the nations two largest ports. But in the macro landscape there have been clear rifts within the ocean freight, and North American trucking industry over the last year and most recently brokers are going under in line with a larger glut in capacity which has been theorized and micro analyzed with the end result being the same, there’s simply too much of it. The problem isn’t as simple as saying the record number of new companies exploding during Covid are falling off stride. That is a real occurrence and a side effect which has implications to us all in some way.

However, if you drill down deeper still you are left with a handful of trend shifts. Consumer demand has been on the reports of nearly all major earnings reports this year, the weakening of consumers’ ability to operate is persistent (as shown in retail trends and outlooks) constrained and they’re all facing higher debt, and higher debt servicing. Record tightening by the FED in response to high inflationary pressures from printing money and easing standards has created a mess, so I wouldn’t trust a substantial input to the freight books via blowout holiday demand, though well-established companies have historically always stood out in value during unstable conditions. Secondly, the volume declines have been in large part from Chinese imports, in mid-September just before the golden week in China the outlook from their end was not great, plus they are forecasting more reductions on the immediate future ( I wrote about this in a previous report) so you can’t count on a lot of volume coming back into the west through one of its biggest counterparties.

While it's true southern and eastern ports have recorded record volumes, along with improvements in the Midwest and adjacent inland regions there has been trouble in managing all the traffic and warehousing. Job creation and investment has been flowing in this year with expansion currently underway in Memphis (a main hub) and in New York and New Jersey (saw some of the biggest volume gains) and the federal government has been allocating its $1.2 Trillion in excess funding for infrastructure projects within the Midwest and south to promote growth in local areas, while also adding major interstate expansion projects to assist with the record $95 Billion in operating costs carriers faced in 2023 (I also wrote about this). These projects are long duration improvements which carry high complexity and take years to complete so there’s little short-term improvements on that end either, though it’s reasonable to assume conditions will improve more gradually into 2024 and beyond.

That circles us back to a single question. Is the transition away from the west into the east permanent, and what implications are needing consideration in the short term. The answer, I think is another question. Are the cost and headcount reductions enough to stabilize the market with a weak economic outlook. Because there are multiple converging trends going into the winter and all of them are codependent on each other in the macro picture, the holiday season, construction, office space, CRE, RRE, are all facing stagnating conditions and play a big role in the freight market in their own way and they are also a direct link to consumers in many ways.

Lastly, the Panama Canal. It’s not entirely surprising the Port Authority overseeing the canal have issued further transit restrictions over the next quarter which will likely add more pressure to the energy markets as energy consists of Liquified Natural Gas, and other petroleum products totaling a third of all transits. The port is key to connecting northeast Asia trade, handling 40% of the trade volumes in the region to various other regions. The effects of the reduction can be managed are often planned for by industry leaders, adding reroutes will add to travel schedules and will lead to cost increases in many areas though until we get into December it’s hard to tell exactly. Though the Canal reductions aren’t surprising their effects are real and the climate agenda doesn’t seem to outline a way those effects can be mitigated other than simply continuing with reductions. So volatility within the system lives on.

The trend toward the southern and eastern regions seem to be an early indication of a greater shift from the Western ports as pricing, nearshoring, capacity reduction, warehousing, and other factors take effect within the industrial complex. While this is good for the Midwest and east, the Western areas have yet to establish a clear outlook other than “we’re stable, but don’t get excited”. Larger economic forces are at play on a consumer level, trucking is facing broker bankruptcies (this coming as carriers also get absorbed), the holiday shopping season accelerates (Amazon and other’s already had rounds of early holiday sales this year so there’s that), CRE/RRE faces persistently higher rates, weakening pricing power/vacancies, and grocery costs are actively being passed onto customers in the form of higher pricing to save profits. All of these things, on top of the previously mentioned credit debt burden on the shoulders of consumers. There are brighter outlooks of course but until the larger trend shows any sort of continuity between improvements, I am saying this winter will be hard on many offering little in the way of clarity or prediction. For industry it will move the goalposts yet again. Some will nail it, some will fall, but everyone is on board.

US Economic Realities: You Can't Always Get What You Want (@GregCrennan, MacroEdge Contributor)

In today's economy, the pursuit of low unemployment and low inflation is seen as possible by many, but the recent economic data suggests that the Government & Federal Reserve's goal of a soft landing may indeed be slipping through their grasp. As the legendary Rolling Stones once said, "You can't always get what you want." Let's break down this week's data to better understand the situation.

Inflation Remains a Thorn in Our Side

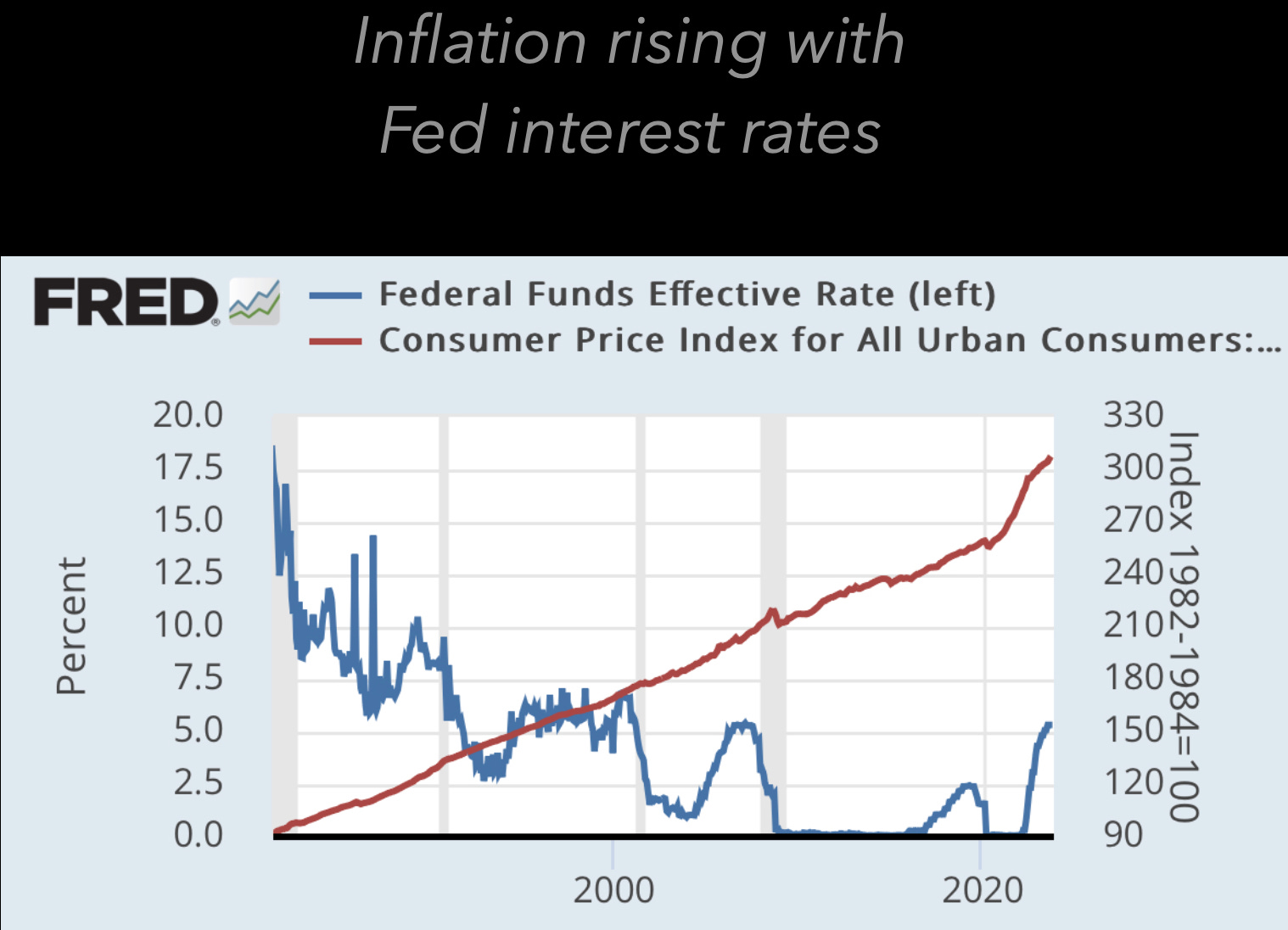

Despite clear signals of ongoing inflation troubles for everyday Americans, the Federal Reserve has chosen not to raise interest rates further above 5.5% or engage in more quantitative tightening(selling of bonds which would raise rates) with the Fed Chair stating that more hikes may be needed to finally eliminate inflation. This reactive stance towards inflation only exacerbates the pain in Americans' wallets, potentially prolonging economic discomfort.

Inflation has not shown any signs of relenting. It's now 4% inching closer to 5% rather than the Fed's target of 2%, causing financial strain and eroding purchasing power for Americans across the board.

Job Market Woes

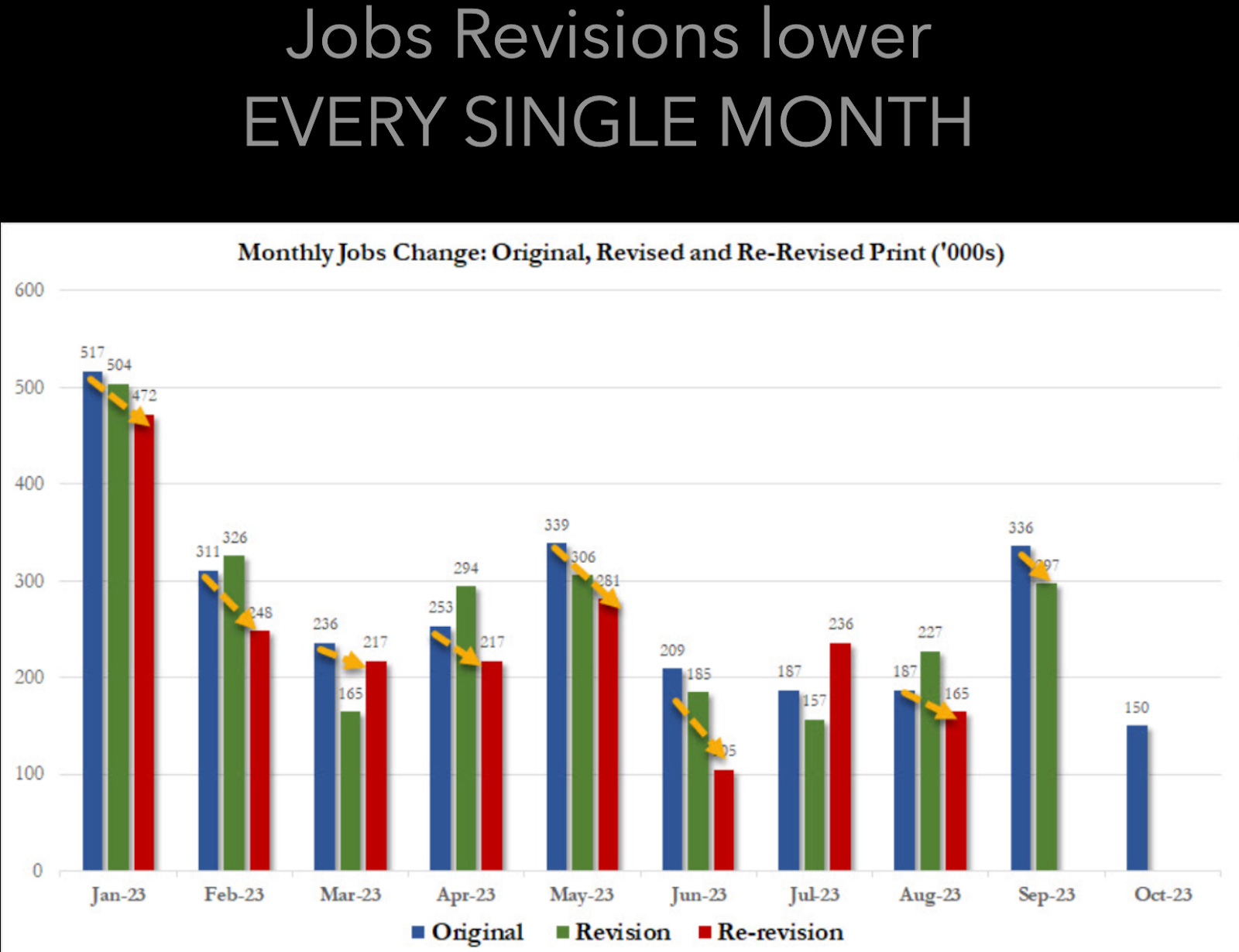

The October jobs report paints a grim picture. To make matters worse, data for the entire year of 2023 has been revised downward, challenging the narrative of a robust economy. August job data was revised from 227k to 165k, and September from 336k to 297k, while October's data showed a further weakening with just 150k jobs added, falling short of the estimated 170k.

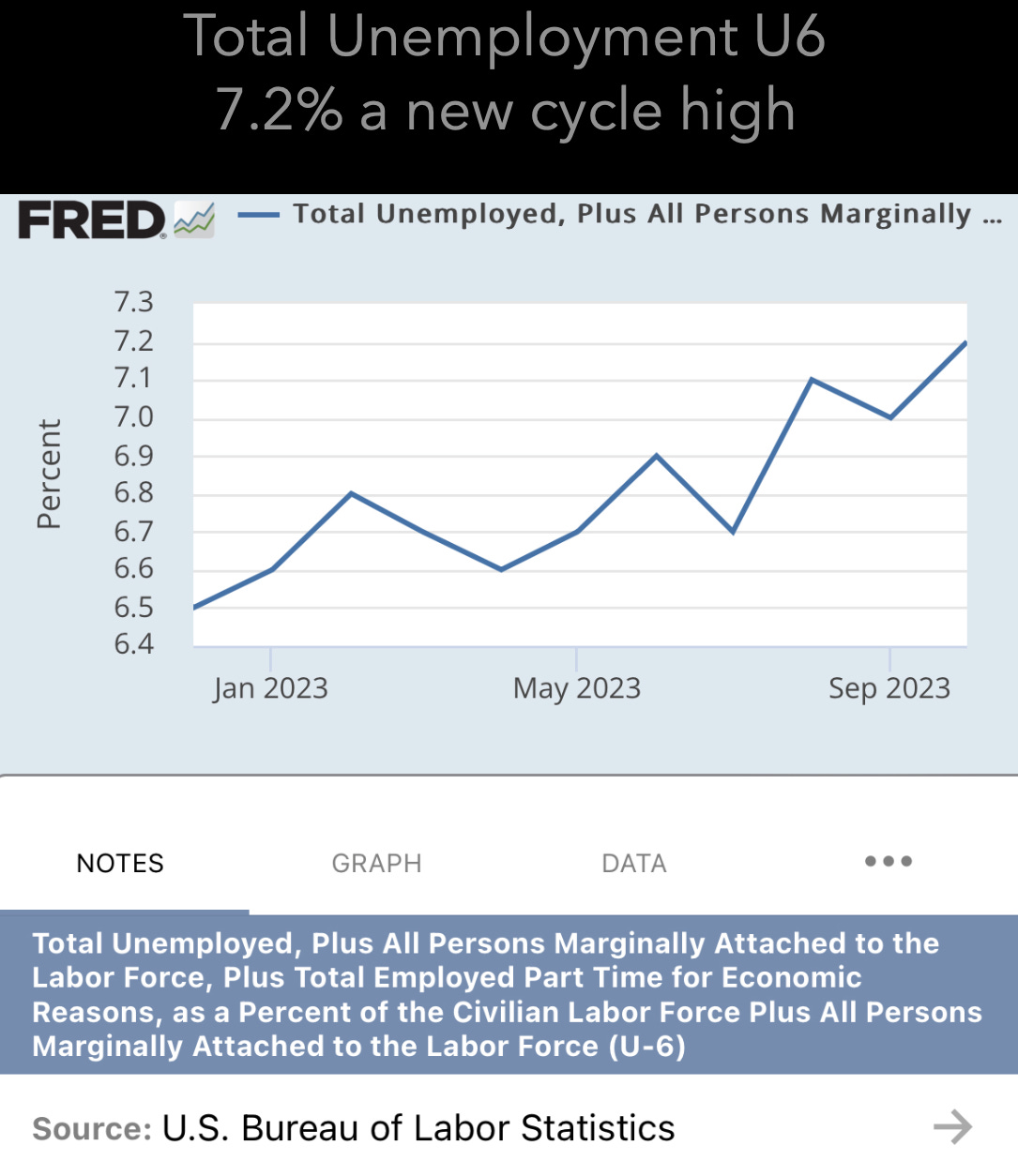

Unemployment is on the rise, and total unemployment U6, a broader measure of unemployment, has reached 7.2%, approaching the highs seen under the Biden administrations. The burden of unemployment and its effects are most acutely felt by African Americans and Hispanics, who are experiencing unemployment rates of 5.8% and 4.8% respectively. This situation contradicts the promises of government policies designed to address economic disparities that include equality for all as our fellow Americans are losing jobs, and now inflation continues to destroy their savings causing overall credit card debt to soar and delinquencies to hit higher levels than when the economy was locked down in 2020.

Tech Giants Falter

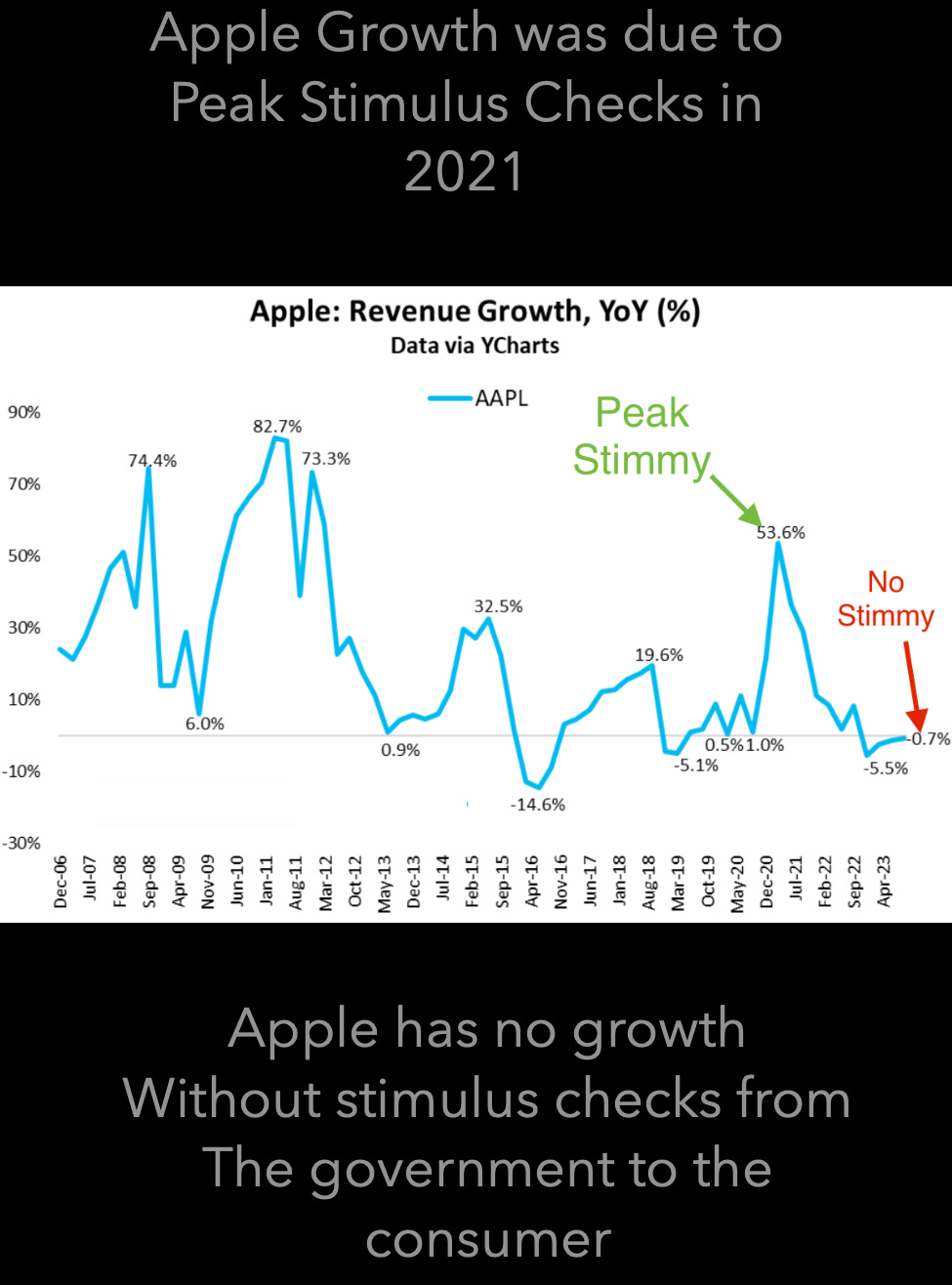

Apple's recent earnings report serves as a gauge for the overall US and global economy. The tech giant reported its fourth consecutive quarter of declining earnings and revenue, a shocking data point to the world's largest company, since this is the first time it happened for the cali tech company, since the bursting of the tech bubble in 2001, signaling a prolonged period of stagnation. This is particularly concerning as they have introduced new products and deals in a bid to stimulate growth. The last time Apple experienced significant growth was due to government stimulus checks in 2021, and since then, their growth has turned into declines and the stock has become overvalued.

As we approach the end of 2023, it's evident that reactive solutions to economic problems are not the path to recovery. While the government and the Federal Reserve have talked about a soft landing, the economic lyrics of the Rolling Stones echo in the background: "You can't always get what you want, but if you try sometime, you'll find, you get what you need." And what we may truly need, given the current fiat monetary system, is a reevaluation and a potential recession.

In the realm of Austrian economics, it becomes clear that the balance between inflation and unemployment is a delicate one, and the Fed's approach may be missing the mark. As we move forward, it's essential to assess our economic strategies and consider more proactive measures to ensure a more stable and prosperous future for all Americans.