11/30 Weekly Macro Note: Light Liquidity Zones, Carry Trade Holiday Volatility, Holiday Shopping Review & Preview, Travel Equities, Metals, Ozone Pro Update, and More

In this Weekly Macro Note, we continue our discussion of the last two weeks on the Carry Trade risks, talk Japanese yields, holiday sales data from Black Friday, look at the looming macro data, & more

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

I hope you all had an enjoyable few days off through the long Thanksgiving weekend. It was a much-needed reset and break from what has been a robust travel schedule to end the year, and I enjoyed the time away from the screens for the few days I was able to spend away from them. Very much looking forward to December now, which is a favorite month of mine, and there is a lot to cover and accomplish through the month.

We’re entering the month on the back of a very expected rally through the Thanksgiving week, on virtually no volume, and thinning liquidity - evidenced by more frequent liquidation events in the crypto markets (something we’re seeing this evening), and a desire by the Fed to pivot to a looser stance than we have at present. On top of that, we’re still seeing some signs at the margin of banking stress in the community & regional banks, as well as in particular funding markets - some of which likely have to do with private credit stress, something that continues to fly largely under the radar for the time being. On top of that, we have metals continuing their breathtaking rally, which I view as a leading warning signal going into 2026 of either much broader macro issues on the horizon (such as credit & employment), or an inflation signal, or a combination of both.

I am expecting that things get more interesting now into the end of the year, with more volatility and a shift away from the complacency mode as we run into the narrative issue again about what the next great or grand thing is enough to push multiples higher & stretch valuations past these all-time high levels. While the Administration has outright stated their goal is to keep equities at/near an all-time high, there’s more nuance to this as the left tail risks grow. The combination of the Carry Trade reload, employment risks, and some echoes of the 07/early 08 trade come back into the equation - another risk off could quickly wipe out this year’s gains due to market cap concentration and concentration risk.

With that being said, let’s get this show on the road and the train on the tracks. For those traveling home today & tomorrow - have a safe day and transit - and I look forward to seeing you for the Midweek Macro Note.

Weekly Macro Preview

Monday: S&P & ISM PMI (Mfg), MacroEdge Job Cuts Tracker (November)

Tuesday: n/a

Wednesday: ADP employment, Services PMIs (S&P and ISM), Industrial data

Thursday: Claims & trade deficit data

Friday:

This is a quieter earnings week, which I think will allow for more volatility over the next couple of weeks. We’re seeing thinner liquidity across global markets - and that was evidenced further by the events with the CME, and some of the liquidations we continue to see in the cryptocurrency space.

Light Liquidity Zones

Equity market liquidity has thinned noticeably in recent weeks, reflected in a decline in average order book depth, wider bid-ask spreads during both the open and close, and reduced displayed size from major liquidity providers. Volumes have softened in key index futures and ETF vehicles that normally carry the load during periods of uncertainty. Large single stock prints are clearing with more price impact than usual, which signals fewer active market makers willing to absorb risk. Price gaps during earnings events, sector rotation days, and macro data releases have become more frequent, which is another sign of a market running on lighter participation.

This environment raises the left tail risk because thinner liquidity amplifies every shock. A modest downside catalyst can produce outsized price moves when fewer buyers stand in the book. Forced selling from funds with tighter risk limits can cascade quickly and pull indexes sharply lower before stabilizers appear. Algorithmic flows that normally smooth volatility instead become accelerants when they detect shallow liquidity, which increases the probability of abrupt dislocations. Markets are still elevated and concentrated at the top, which means even a small reversal in megacap sentiment can cause an exaggerated drawdown in an illiquid backdrop.

Holiday Volatility

As we head into the holidays, we outlined the remaining ‘TACOs’ in the Weekly Macro Note last weekend - and noted how the narratives for continued mass speculation and gambling in this environment are thinning as unemployment rises. While we’re open to an abrupt change in the direction of employment and inflation, the risks are still right there, and there’s got to be a reason other than narrative and speculation to justify permanently higher valuations if we’re expecting the *permanently high plateau*.

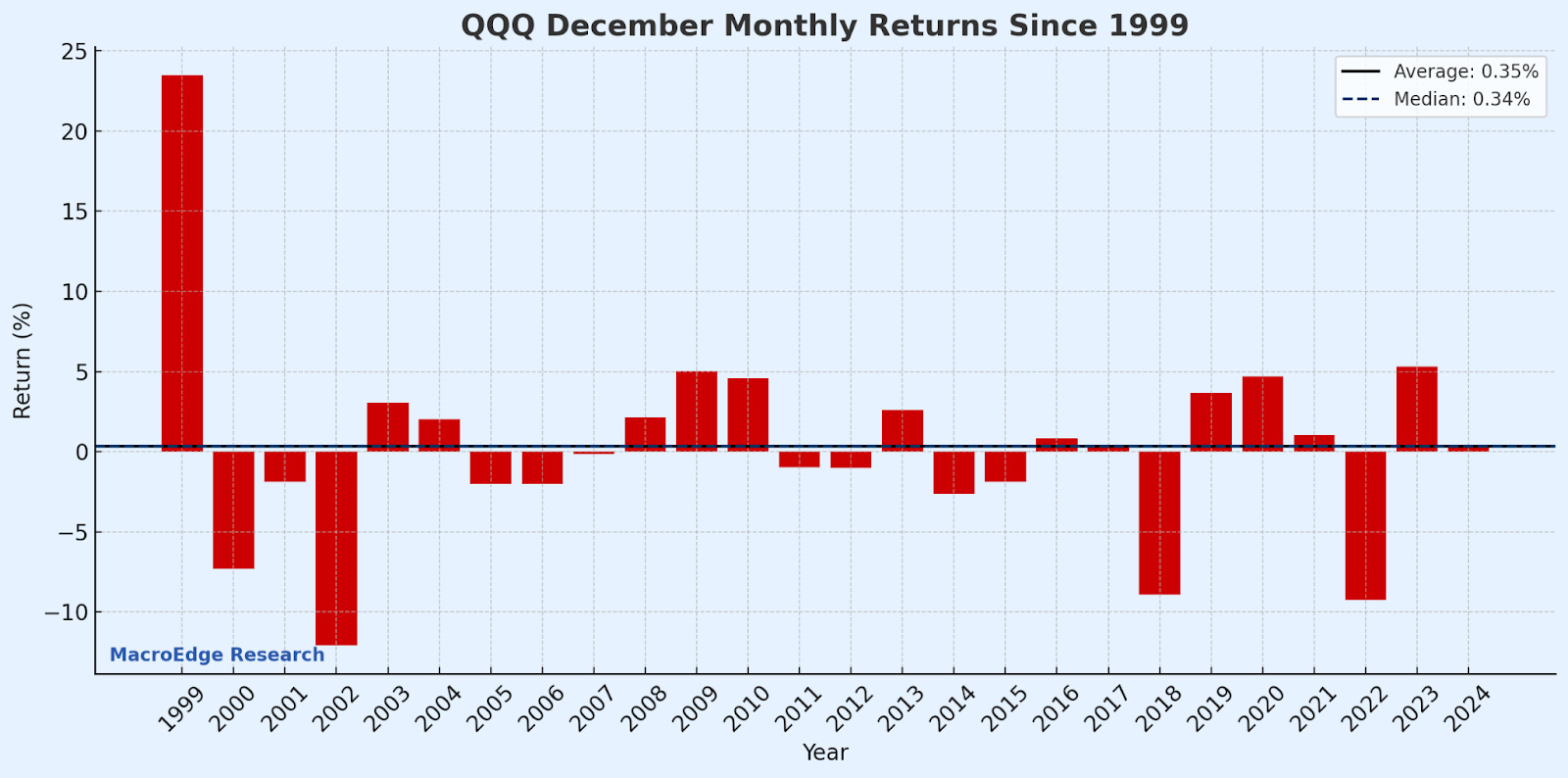

December over the last 25 years hasn’t been as pro-Santa rally as we might expect, looking at sentiment on X:

VIX fell back to a more sustainable reset zone, while the put-to-call ratio on the short trading day hit one of its lowest readings of the decade. Until our Bitcoin / QQQ correlation breaks down, we can continue to use Bitcoin as the leading financial conditions index for high beta & more.

Holiday Shopping Review and Preview

Early Black Friday data points to a mixed consumer environment. Online sales have held up reasonably well with steady demand for electronics and home goods, which keeps the headline spending figures looking stable. In-person traffic tells a different story with footfall down 3.9 percent year over year across major malls and retail corridors, a sign that discretionary shoppers remain cautious. Nominal sales are being supported by higher price points and stronger luxury goods performance rather than broad-based unit growth. The picture that emerges is one where spending levels can appear healthy on the surface, but the underlying volume of goods moving through the system is softer and increasingly concentrated in higher-income segments.

Real retail sales will tell us the *real* story when released, as nominal figures have largely just become an inflation peg:

Travel Equities + Metals

I wanted to briefly look at the airlines & cruise equities given that I’ve put the TSA travel data back on our radar through the remainder of the year. Airline equities had a strong close last week, but have been rangebound for the better part of the year. Without a close to new highs, this could be a solid opportunity to look for downside of data softens and ‘peak travel’ is confirmed - especially among the Millenial & GenZ cohorts - who are facing financial strain across the board and are more ‘asset light’ than the X/Boomer/Silent cohorts that will likely continue to travel as long as equities remain elevated.

Cruise stocks, unlike airlines, have established a more bearish trend in recent weeks - with one notable player (RCL) consolidating now below the weekly (50), something it hasn’t done since 2023. With the candle of last week and downside from here, this could be setting up for a retest of the April lows, and potentially lower to the 200.

(continued below - gold and silver) - access all of our reports & more with two week access below:

subscribe thru Substack:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.