11/26 Weekly Report: US Economy: Navigating Mixed Signals and Thanksgiving Market Insights: Volatility, Earnings, and Argentina's Anarcho-Capitalist Surge

@DonMiami3, MacroEdge Chief Economist; @SixFinance, MacroEdge Head of Research

US Economy: Navigating Mixed Signals (@DonMiami3, MacroEdge Chief Economist)

The US economy continues to exhibit mixed signals, with some data points suggesting a potential slowdown and others indicating continued growth. Despite the ongoing uncertainty, the US economy remains resilient, underpinned by strong consumer spending and a robust labor market.

Persistent Labor Market Strength

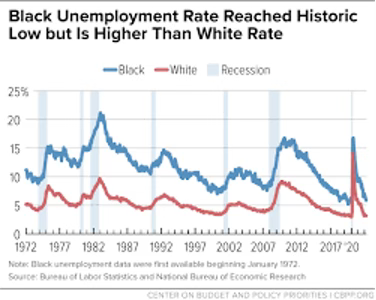

The labor market remains a bright spot in the economy, with unemployment hovering near a 50-year low of 3.9%. The latest jobless claims data showed a slight increase in initial claims, but the four-week moving average remained near pre-pandemic levels.

Unemployment Rate

Center on Budget and Policy Priorities

The strong labor market is being supported by solid job growth and a low quit rate. However, labor shortages persist in some industries, and concerns about a potential recession could dampen hiring in the coming months.

Job Cuts Tracker to Remain Low

We expect our MacroEdge Job Cuts Tracker data to remain less than the October headline number seen in our job cuts tracker. This suggests that companies are still relatively hesitant to lay off workers despite the economic headwinds.

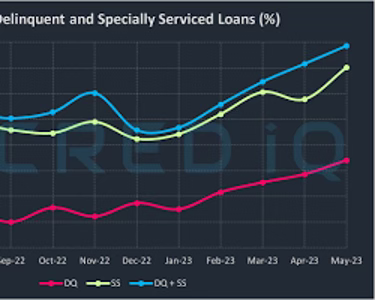

CRE CMBS Special Servicing Rate Stabilizes

The CRE CMBS special servicing rate, a measure of commercial real estate (CRE) loans in distress, has stabilized in recent months. According to data from CredIQ, Trepp, and BisNow, the special servicing rate stood at 5.5% in October, down from a peak of 7.4% in April 2020.

E CMBS Special Servicing Rate

The stabilization in the special servicing rate suggests that the CRE market is improving. However, it is still too early to say whether the market has fully recovered from the pandemic.

Manufacturing Activity Shows Signs of Resilience

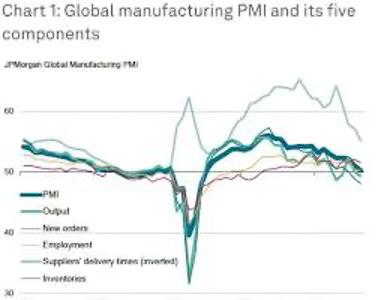

The manufacturing sector, a crucial component of the US economy, demonstrated resilience in November, expanding for the tenth consecutive month. The S&P Global Manufacturing PMI registered at 50.2, slightly below the October reading of 50.4 but still above the 50-threshold that separates expansion from contraction.

S&P Global Manufacturing PMI

The uptick in manufacturing activity was supported by a modest improvement in new orders, which rose for the first time in five months. However, supply chain disruptions and labor shortages continue to pose challenges for manufacturers.

Full MacroEdge Weekly Report only available at MacroEdge.net.