11/12 MacroEdge Weekly Report - The Winter Lull and The 30 Year US Treasury Bond Auction Failure that Wasn’t But Was.

11/12 Substack MacroEdge Weekly Report

@DonMiami3, MacroEdge Chief Economist

@RealJohnGaltFla, MacroEdge Contributor

The Winter Lull (@DonMiami3, Chief Economist)

Happy almost Thanksgiving week everyone - one more week to go. Things are quieting down around town a bit as people go into holiday mode - also seeing this in our data. Today’s focus will be a quick look into expected holiday travel and oil demand, our bellwether Nevada employment data, and a quick ‘look ahead’ at the next two months.

Starting first with our quick look ahead - it’s anticipated that the GOP-led House will pass another stopgap measure to keep the government funded through January. While this measure will add almost $2 trillion to the national debt by March of next year - the endless ‘fiscal howitzer’ continues to fire relentlessly against the Fed trying to tighten. The result of this is likely to be continued elevated yields if the economic data remains resilient. The sharp drop the other day in yields highlights the volatility in the bond market currently (I am expecting both volatility and elevated yields to persist). The equity market itself has made a monster move higher in the last 10 days and this may continue if economic resilience continues (coupled with the House successfully passing their stop-gap measure, which has not yet happened). The CPI, employment data, and retail sales data stand out as points this upcoming week that we’ll be discussing next weekend.

Turning our attention toward expected holiday travel in the United States (along with expected holiday spend) - a few notable points stand out from the Deloitte Holiday 2023 Travel Report:

“Nearly half the country plans to travel between Thanksgiving and the middle of January, according to the 2023 Deloitte Holiday Travel Survey. They’ll be traveling less frequently, though, meaning the concentration of people taking a trip around Thanksgiving and the week between Christmas and New Year’s Day is going to be higher.”

“More than one-third of travelers (37%) will take a flight at least once this holiday seasons. Roads, though, might be a bit less congested, as 53% of American travelers are planning road trips, compared to 64% last year.”

“The travel industry is reaching its cruising altitude this holiday season,” said Mike Daher, vice chair, Deloitte LLP and U.S. transportation, hospitality and services non-attest leader in a statement. “Spending time with family and friends is even more important during the holidays, and Americans are embracing this tradition as they pack away many of the concerns that impacted plans last year.”

“The big beneficiary of this travel boom could be hotels. Some 56% of holiday travelers say they play to stay at a hotel at some point in their journey this year, compared to just 35% last year. The average traveler expects to spend $2,725 on their trip, Deloitte reports.”.

The takeaway here is that spending is up year over year even though the # of true travelers deterred by higher costs is always much higher. The financial strain of higher inflation is clearly impacting the bottom 50% the most - and surveys like this make this clear. The beneficiaries of this looming holiday blowout are likely to be the hotel sector, airlines, as well as oil companies - but we’ll have to watch the data closely to see how the survey compares to the reality that materializes over the next 6.5 weeks. Airlines that have been crushed of late in the markets may see some reprieve from this expected “cruising altitude” holiday season that Mike notes above.

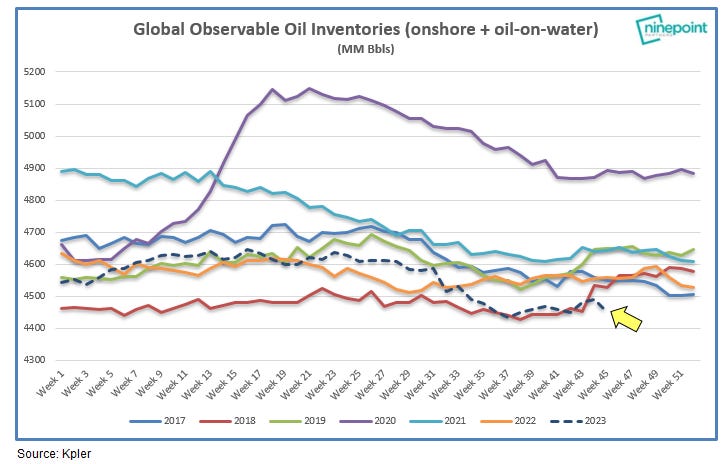

On oil demand - oil inventories (below) remain very suppressed from previous years, per Ninepoint Partners in Canada:

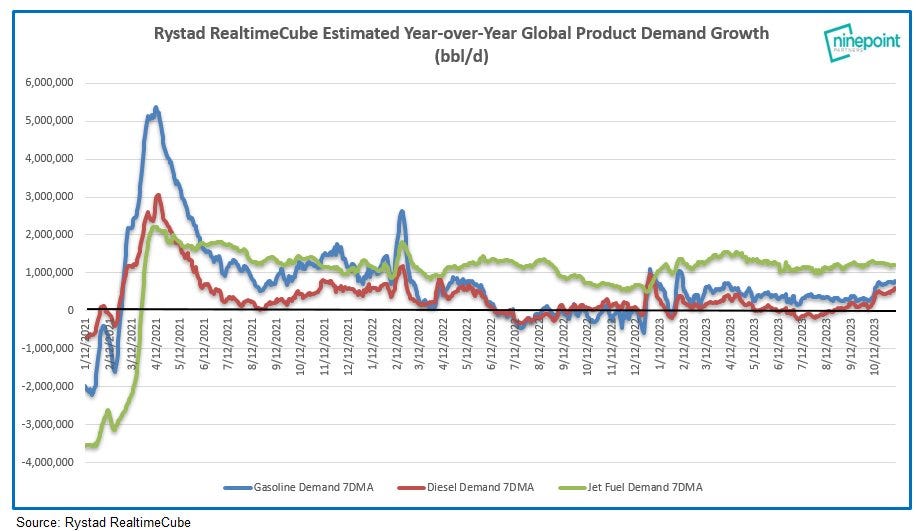

Jet fuel continues to remain robust (above) - as does gasoline and diesel demand. The divergence between the real-time data and the EIA data is becoming increasingly interesting and backs up the notion that the physical oil market is extremely tight while the financial one is not so tight. The oil and gas sector - like other sectors above - may be another beneficiary of a ‘cruising altitude’ holiday season. An ETF that I’ll be watching closely over the next few weeks is PSCE.

Have a great evening and start to your week.

[View full report by joining us at MacroEdge.net]

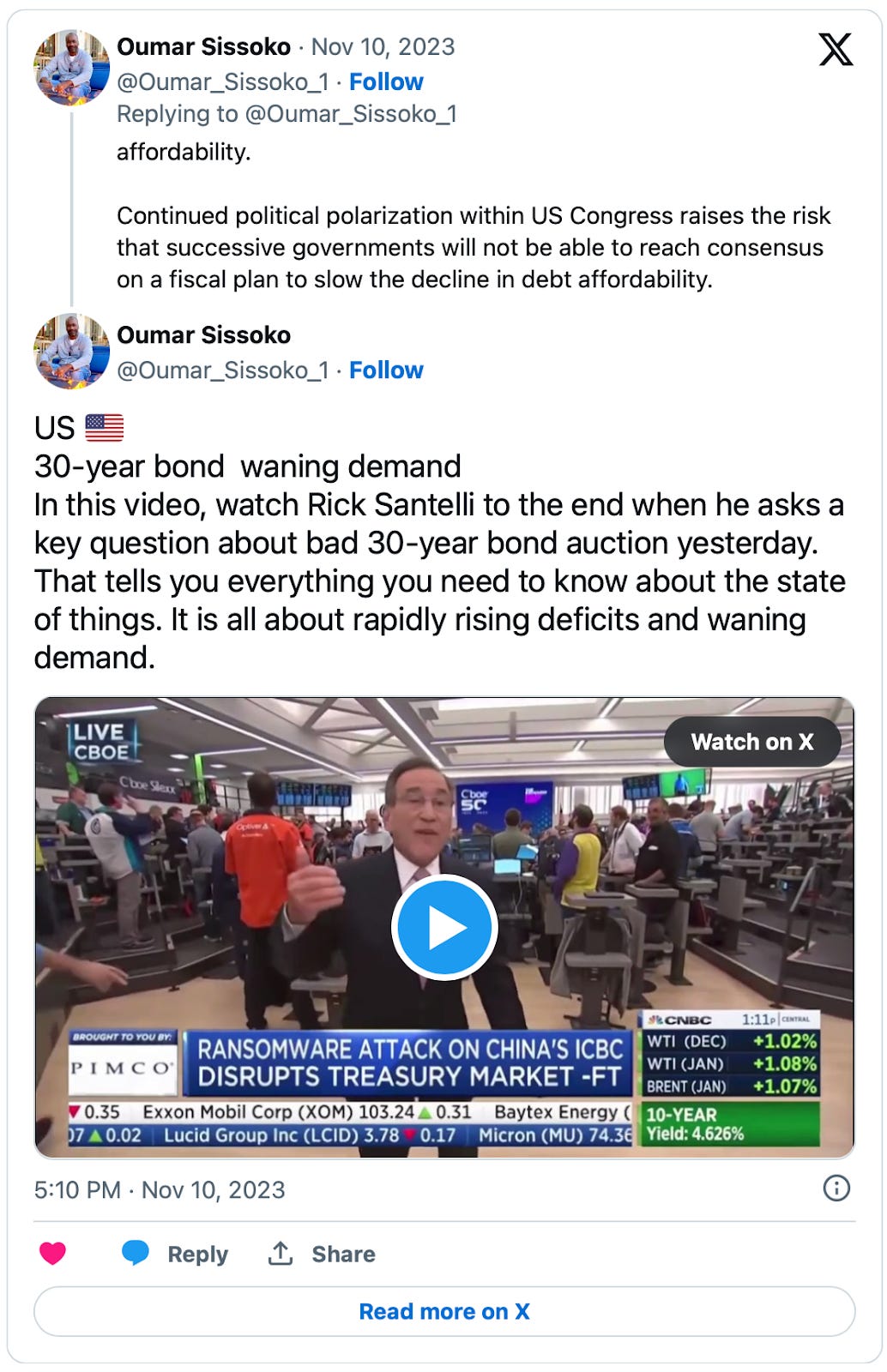

The 30 Year US Treasury Bond Auction Failure that Wasn’t But Was. (@RealJohnGaltFla, MacroEdge Contributor)

On Thursday, November 9, 2023, the United States Treasury department under the sterling leadership of one Janet Yellen got a taste of what a failed US Treasury bond auction would look like. The solution to the problem?

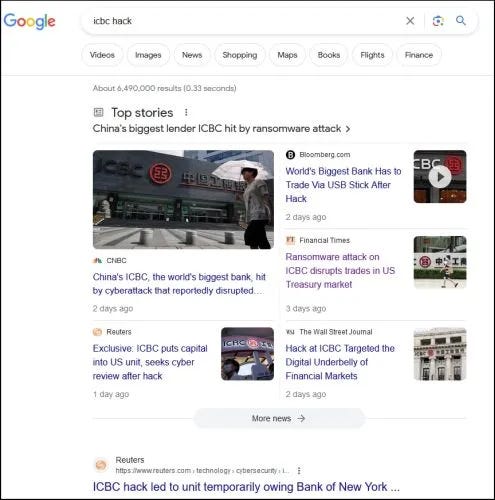

Blame a nebulous hacker that allegedly infiltrated a major Chinese financial institution for the problem.

Via Bloomberg TV: ICBC Hack Unfolded at Critical Point for Treasury Market

And if any of my readers believe that, I have some gold plated tungsten bars from Xinjiang to sell you as 24K gold bullion.

The media immediately ran with the US Treasury and Federal Reserve narrative:

I’m not saying there were not hackers. But the “drama” pushed by the financial bubble visions in America to cover for what really was a failed auction really speaks volumes to just how fragile the US financing system for our government truly is.

In fact the Reuters story at the bottom of the screenshot above makes this sound like the world was coming to an end per this excerpt:

“Industrial and Commercial Bank of China’s hack left its U.S. unit temporarily owing Bank of New York Mellon $9 billion as a result of unsettled trades, prompting the parent to inject capital into the unit to settle the trades, sources familiar with the matter said.

BNY has since been paid back, the sources said.

The attack, confirmed by ICBC on Thursday, is the latest in a string of ransom demands by hackers this year. ICBC Financial Services, the bank’s U.S. unit, said on Thursday it was investigating the attack that disrupted some of its systems, and making progress toward recovering from it.”

Note this part of the story: “the sources said.”

No direct quotes. No factual presentations. Just “yeah were were hacked” but “yeah we made good.”

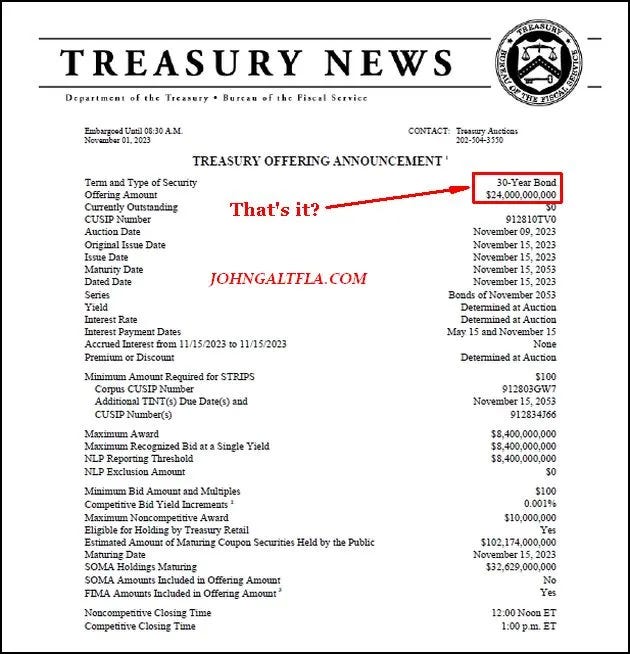

But $9 billion of unsettled trades is not enough to actually influence a 30 year US Treasury auction which was only $24 billion in total was enough to derail an auction?

This brings up the big question:

Why the narrative to divert attention from a lack of demand?

Bond markets, like equity markets, are built on confidence of either future growth (equities), or the future ability to settle or pay debts as issued via bonds. If the world, or the US investing community loses faith in the bond market, things get very messy, very, very, fast.

Rick Santelli gave it the perfect grade and without saying it was a failed auction, gave it a D- for a grade which is the polite way of saying, it was a failed auction.

Thus the reality is why blame the Industrial and Commercial Bank of China on a failed bond auction?

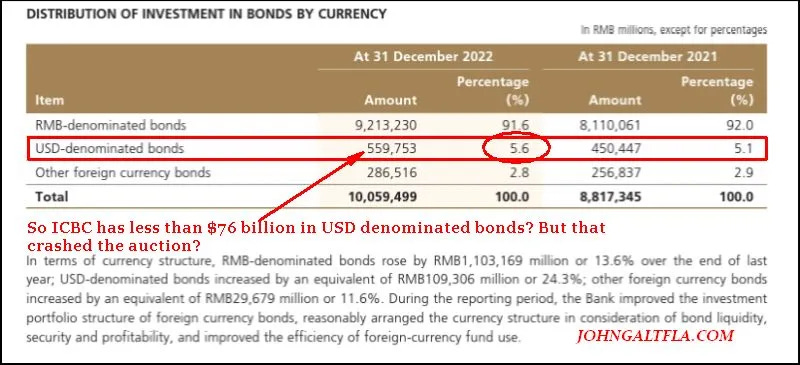

Let’s lift the hood on this sucker and see why. If one actually spends more than 3 seconds of their attention span and READS the ICBC annual financial report, one would realize they really are not as big a player in the US Treasury market as one might think.

The ¥ 559,753,000,000 in US denominated bonds on hand at the end of 2022 is 5.6% of their entire portfolio. As illustrated above, that is only $76 billion dollars which includes corporate bonds, MBS (Mortgage backed securities-probably leftovers from over a decade ago) and other dollar denominated instruments.

The reality is that the Chinese banks are reducing their holdings of US denominated bonds, especially corporate issues, but still rolling over US bonds into T-bills and shorter denominated issues.

Thus the bubblevisions are trying to push the narrative that the lack of demand for US Treasury bonds was not due to inflation and the loss of faith in the Federal Reserve and our Political leadership, but due to a “hacker” creating a processing problem for transactions between Wall Street and Beijing.

If one wants to continue believing in sunshine and lollipops, please go right ahead. But with primary dealers taking down almost 25% of this week’s auction, it was a failure in everything but name only.

Buckle up, the turbulence is about to get far, far worse as the Fed’s most recent blunder will cost the markets far worse than missing two 25 bps rate increases to contain the upcoming inflationary outburst ever will.