10/8 Weekly Report - 'Bubble Made of Cement, the Fed Ahead, Job Data Deep Dive, Bond Market Woes, and More'

In this weeks MacroEdge Weekly Report - Don, Six, Joe, Greg, and John take on everything from the 'bubble made of cement', the latest BLS jobs report, the current Israel instability, bonds, and more.

10/8 MacroEdge Weekly Report

@DonMiami3, MacroEdge Chief Economist

@SixFinance, MacroEdge Head of Research

@SquirtLagurtski, MacroEdge Contributor

@GregCrennan, MacroEdge Contributor

@RealJohnGaltFla, MacroEdge Contributor

Weekly Data Update and the Bubble Made of Cement (@DonMiami3, Chief Economist)

Another Sunday evening all and here we are - what a wild week and weekend of events that have all occurred since we last spoke last weekend. I am preparing to take our week long research trip out to Nevada so will be keeping my piece fairly short for the week but will quickly talk about the new global geopolitical issues in the Middle East with the Palestinian invasion of Israel, discuss our latest update to the MacroEdge Leading Economic Index, cover the latest update on the SPX vs 10 year 3 month inversion curve correlation, & discuss the continued (long) lag we are seeing this cycle as the 10y/3m remains steeply inverted at -72 basis points. If you would like to join the pre-access list for MacroEdge Ascend Weekly Research Reports and our O3 (Ozone) Data/Insights Dashboard - you can now do so at: https://www.macroedge.net/

- and scroll to ‘individual’ or ‘collaborative’ to fill out a request form. We will be approving individuals/companies on a case by case basis over the month of October.

Regarding the Israeli-Palestine conflict - I anticipate there to be at least some short term volatility from this event (we’re already seeing a little in the futures and even moreso in oil) but not sure this event alone is enough to spook markets unless a major player becomes directly involved… ie: Iran, etc. The bigger risk to the international markets will be on the oil price front if the conflict widens and then we may begin to see further upward oil price pressures although I still don’t see this as a catalyst for the $100+ oil that many analysts are currently calling for. The conflict is yet another representation of the growing fractures in the world and evidence of the fact that history will continue to repeat itself over & over again because we as humans cannot seem to ever help ourselves. Even Fed Chairwoman Bowman acknowledged possibly issues from rising geopolitical tensions which I believe is something Six will discuss below.

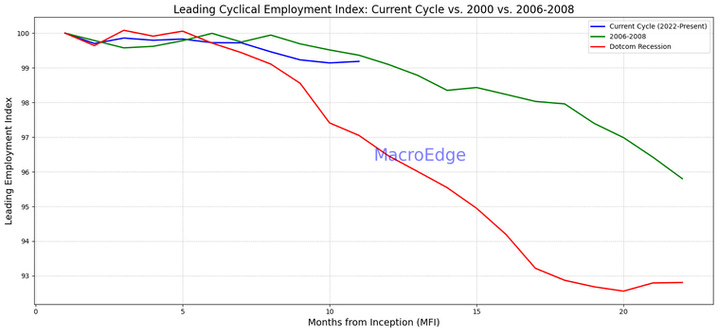

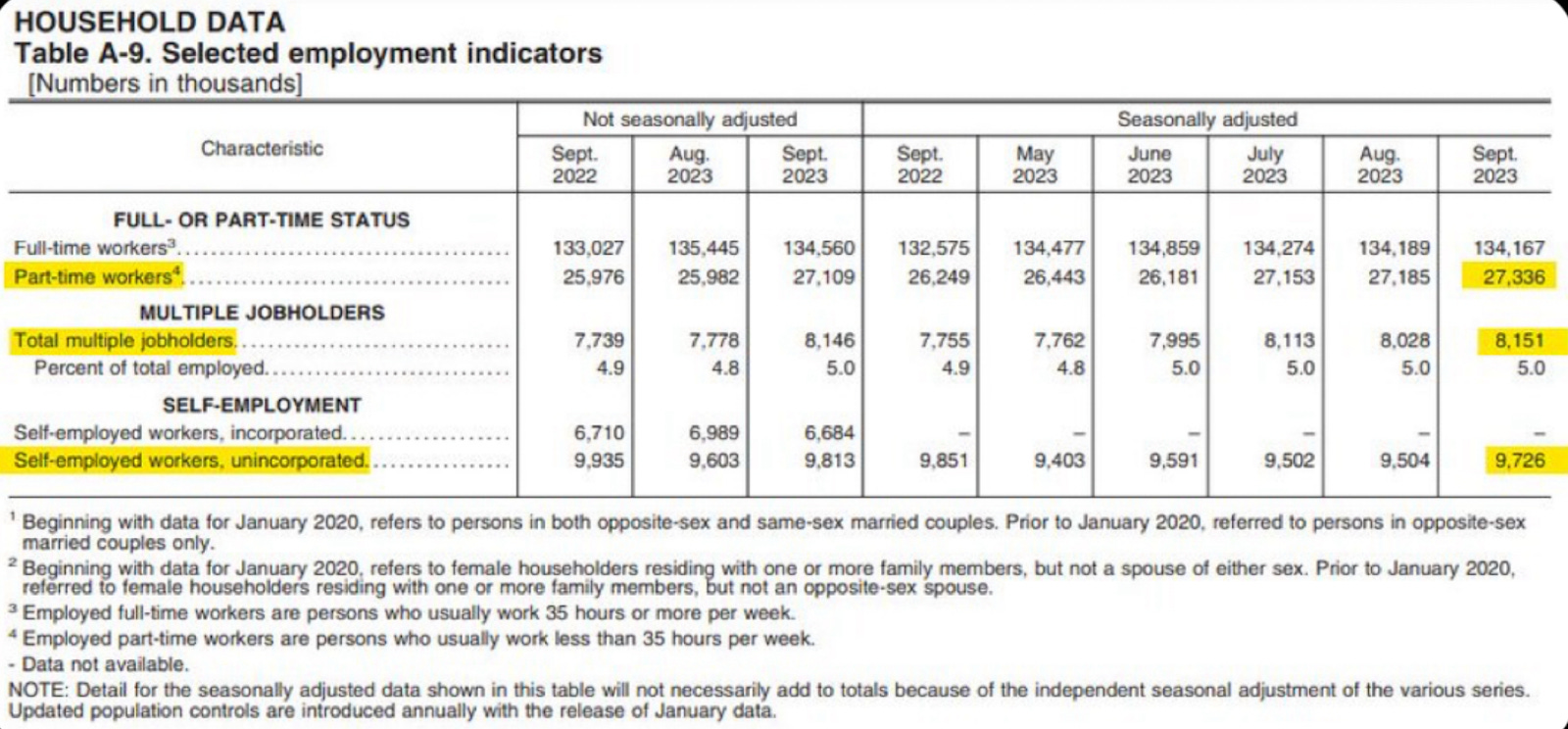

Turning towards the labor market - we got another very solid headline print adding over 300,000 new jobs to total nonfarms, although total full time jobs contracted on the aggregate off 22,000 month to month while most of the job growth came from part time employment in hospitality/service and the government sector. A few of my tweets garnered very large attention when I pointed out the actual ‘weak’ nature of this jobs report. The jobs report for a society points to weakness - especially when you see an all time record of individuals taking on a second full time job just to get by in our world that grows more and more expensive by the month as our national debt continues to balloon w/no debt ceiling and no House Speaker in sight. Our MacroEdge Cyclical Leading Employment Index, which uses an average sector methodology of 7 very cyclical sectors (construction, technology, HR service, temp help, hospitality, retail, and manufacturing) actually saw a very small bounce month over month on the stronger jobs print. With the curve remaining this inverted still at this point in the cycle - the next 2-3 months may be a continued flatline or slower grind lower for our Leading Employment Index as things continue to weaken within some of these sectors. While manufacturing employment growth remains strong - I would anticipate that the remainder of this quarter will see further headwinds in the construction employment sector - especially on the real estate front. Technology, HR service, and temporary help employment markets continue to weaken fairly rapidly which is something we often see well in advance of the recession ‘start’ as backdated by the NBER.

As stated above - the next 3 months will be interesting to watch employment movement within the most cyclical sectors of economy - but I do anticipate that come early December/Jan we do see this Index lower than it stands now.

Current Index: 99.1859 versus 99.14095 (seasonally adjusted)

On the job cut tracking front - we stand just above 17,000 at this point in October, which is about a 200% increase month over month for the first 8 days of the month… Something to definitely watch as the UAW strike rolls on and we likely get figures on the size of the bank/consulting sector layoffs in the months to come.

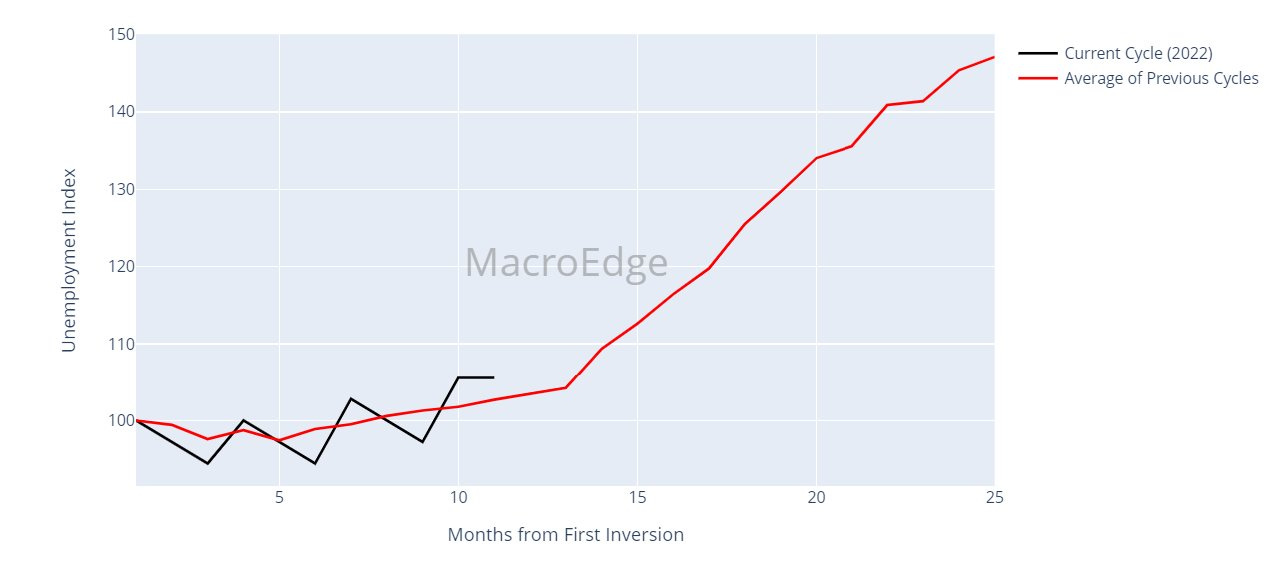

Our unemployment index for this cycle continues to track closely to the average of previous cycles and should remain in the 3.7-4.0% range over the next 3-4 months:

Labor giving it’s very lagging nature will be the ‘last’ piece to show a true slowdown and has remained remarkably resilient in lieu of a lot of headings. If equities face pressure into the winter, we may see technology sectors & other individual names trading at extreme P/E ratio’s begin to pullback on the number of employees they see as necessary going into H1 2024. Our continued base case is that we see the labor market begin its rollover in the latter half of this quarter thru sometime in Q1 - although this will be updated as more data comes in over the winter.

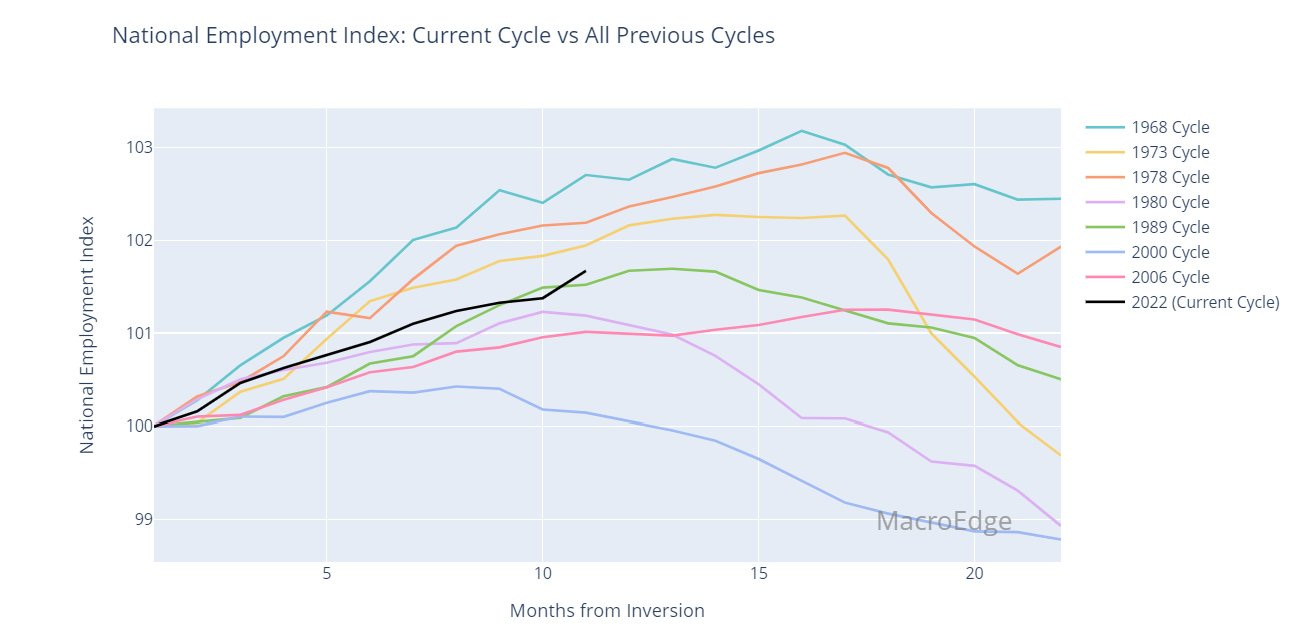

Aggregate payroll growth remains strong at this point in this inversion cycle (above).

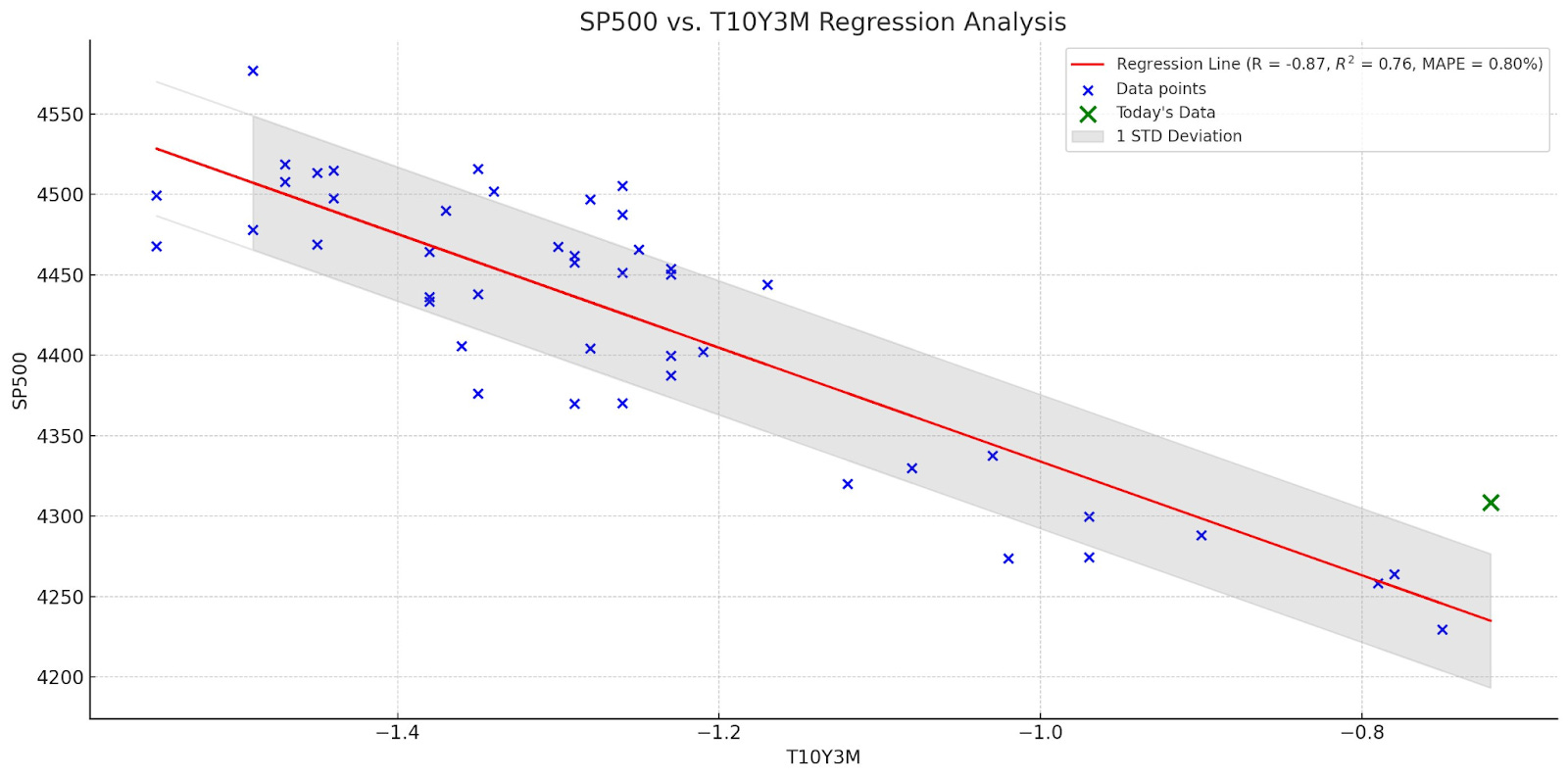

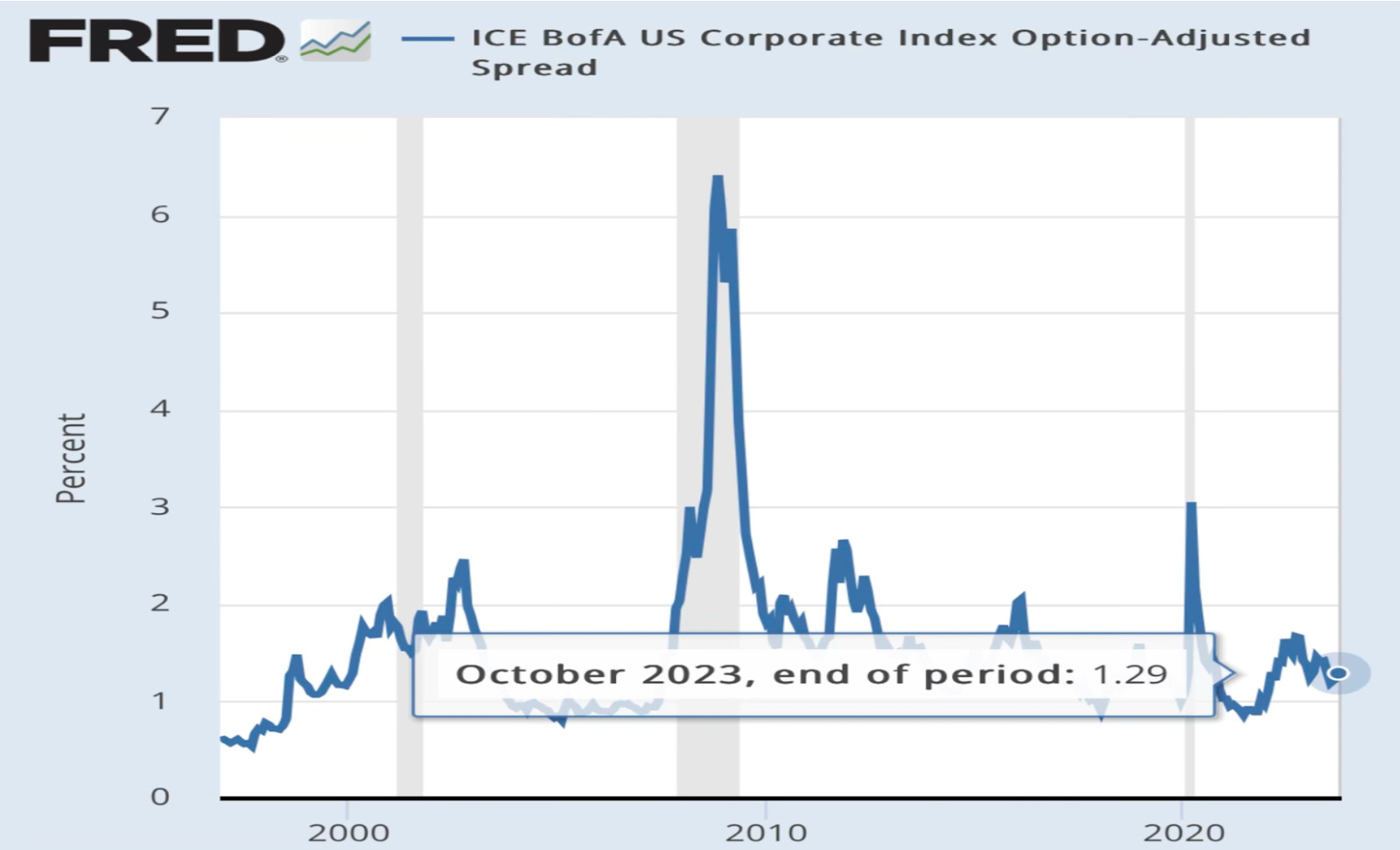

Turning quickly to the S&P500s relationship to the ‘steepner’ occurring with the 10y3m curve - which is seeing a quick rise from very negative levels towards 0, now at -72bps, there continues to be an interesting relationship to watch here over the next month. I anticipate that the event with yields may not be done yet even as analysts anticipate the bottom to be in for the long bond (‘buy TLT’ they say)... that trade will eventually be a winner when the Fed does make the decision to cut rates but for now the tone remains hawkish & yields are doing the leg work of another ‘hike’ for the Fed. As long as the trend continues here - no change in anticipation of yields rising a bit. Friday’s print on SPX was nearly an outlier on the larger trends since the beginning of August:

I noted on X that this is something to watch at it has been a ‘fakeout’ signal in 8/9 instances this has occurred where the yield curve steepens towards zero and SPX prints a strong positive day. Will this time be different?

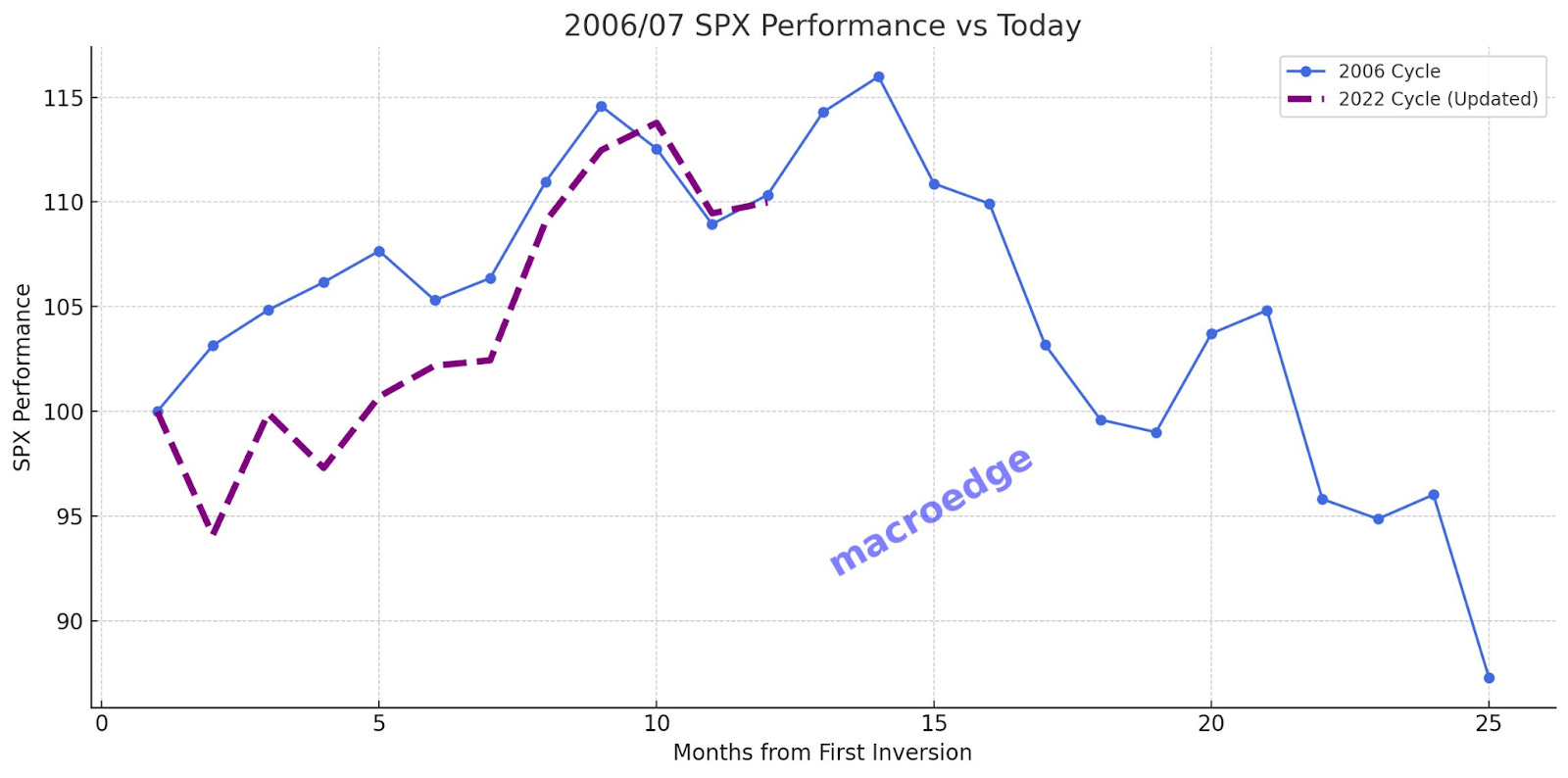

SPX also continues to closely track 2006-07 cycle following inversion, even though it will likely surpass the length of inversion of that crisis (which is why we anticipate a significantly long downturn >9 months when it does begin).

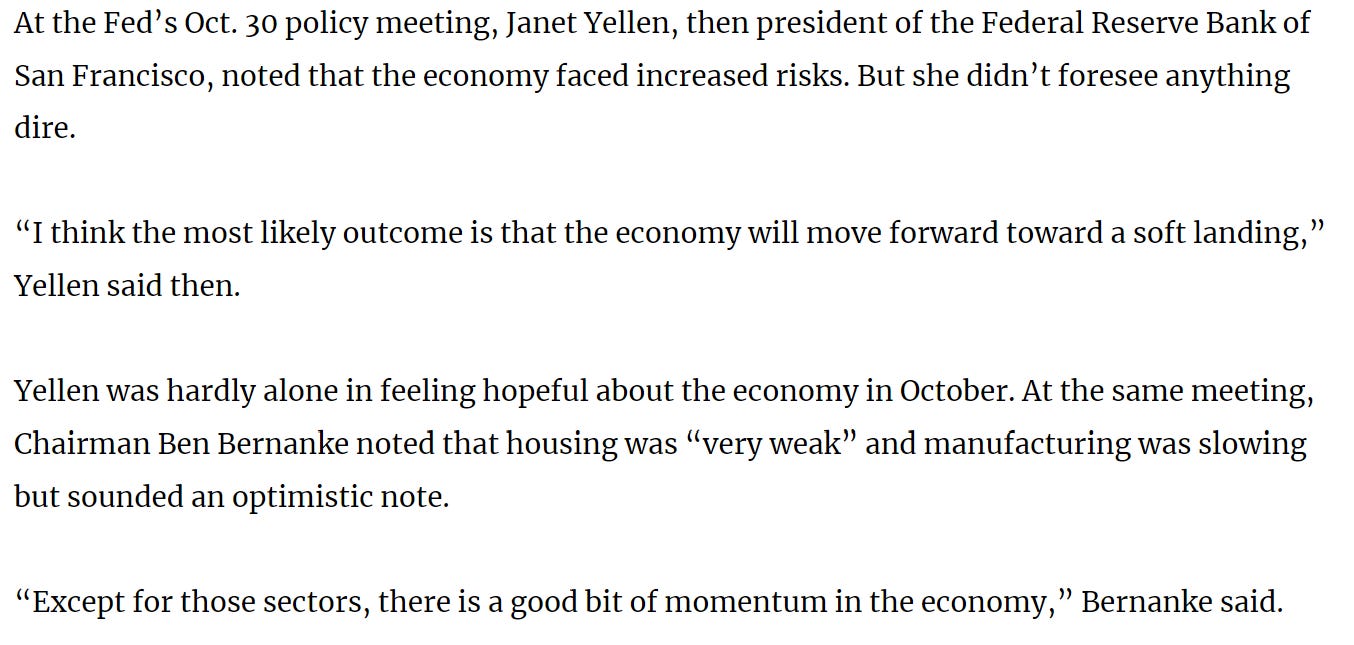

Regarding the lag of this cycle following unprecedented soft landing/optimistic headlines about the state of the labor market, etc - let me just remind you of Yellen & Bernanke’s opinion on the economy in October of 2007 (fewer than 2 months before the Financial Crisis began):

We continue to err on the side of great caution about this ‘Bubble Made of Cement’ as the article title implies - and the risks for this economy and bubble party lean greatly to the downside over the next 12 months.

Have a great evening all and enjoy the rest of the great pieces from our team below!

See you again at 35,000 feet.

Don

Oh p.s. and last point about cement. A lot of times it may look strong, but in the end it comes crumbling down… just as bubbles go pop.

An Eventful Week Around the Globe and ABNB Update (@SixFinance, MacroEdge Head of Research)

Extremely eventful week. It appears we are now entering the final phase of the economic cycle.

Early Saturday morning Hamas from Gaza launched an attack on Israel, launching thousands of rockets into Israel and invading with ground forces slaughtering hundreds of civilians. Israel declares war. Reports that Hezbollah from Lebanon are also launching attacks into Israel. We will have to watch this carefully and see how it develops.

Oil prices plummeted Wednesday with /CL futures down over 5% on report that US 4 week rolling demand was down to the lowest levels since the 90s.

10 year yield hits a new cyclical high on friday and then comes way off early in the day followed by a strong close at roughly 4.8% This was on the heels of a blowout NFP number on friday in which 336k new jobs were added beating expectations of 170k. The report was slightly misleading however as a large part of those new jobs added were second jobs, and likely gig employment. A large influx of new government jobs also aided the report. Private sector full time employment fell by over 400k jobs.

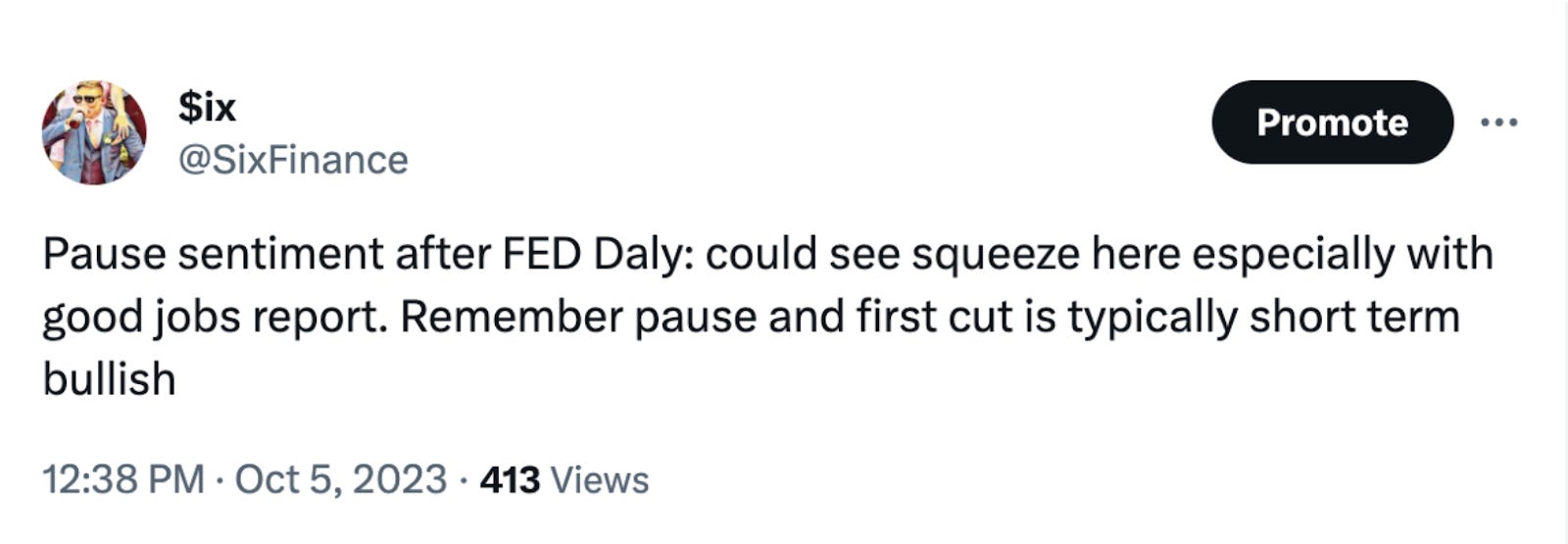

Mary Daly, San Francisco FED President, affirmed our thoughts about a final rate hike being unnecessary due to the long end of the yield curve doing the tightening for them. A blowout jobs number did in fact materialize an aggressive rally on Friday.

It is unlikely in my view that we see another hike in November but anything is possible

USDJPY climbed again this week to 150 per USD before a sharp drop from 150. The Bank of Japan clearly intervened as they refused to give comment. USDJPY already is back on the approach to 150. With inflation elevated in Japan and the Yen continuously testing their 150 intervention level it remains very possible that Japan will be forced to abandon their long standing policy of yield curve control and abandon negative interest rates.

As we enter the late cycle I will be putting on the long IEF short HYG pair trade. I expect credit spreads to widen substantially from here and see very low risk yet high reward in putting this trade on. Credit spreads are far too tight considering the plethora of Macro risks as well as the tightening of credit conditions.

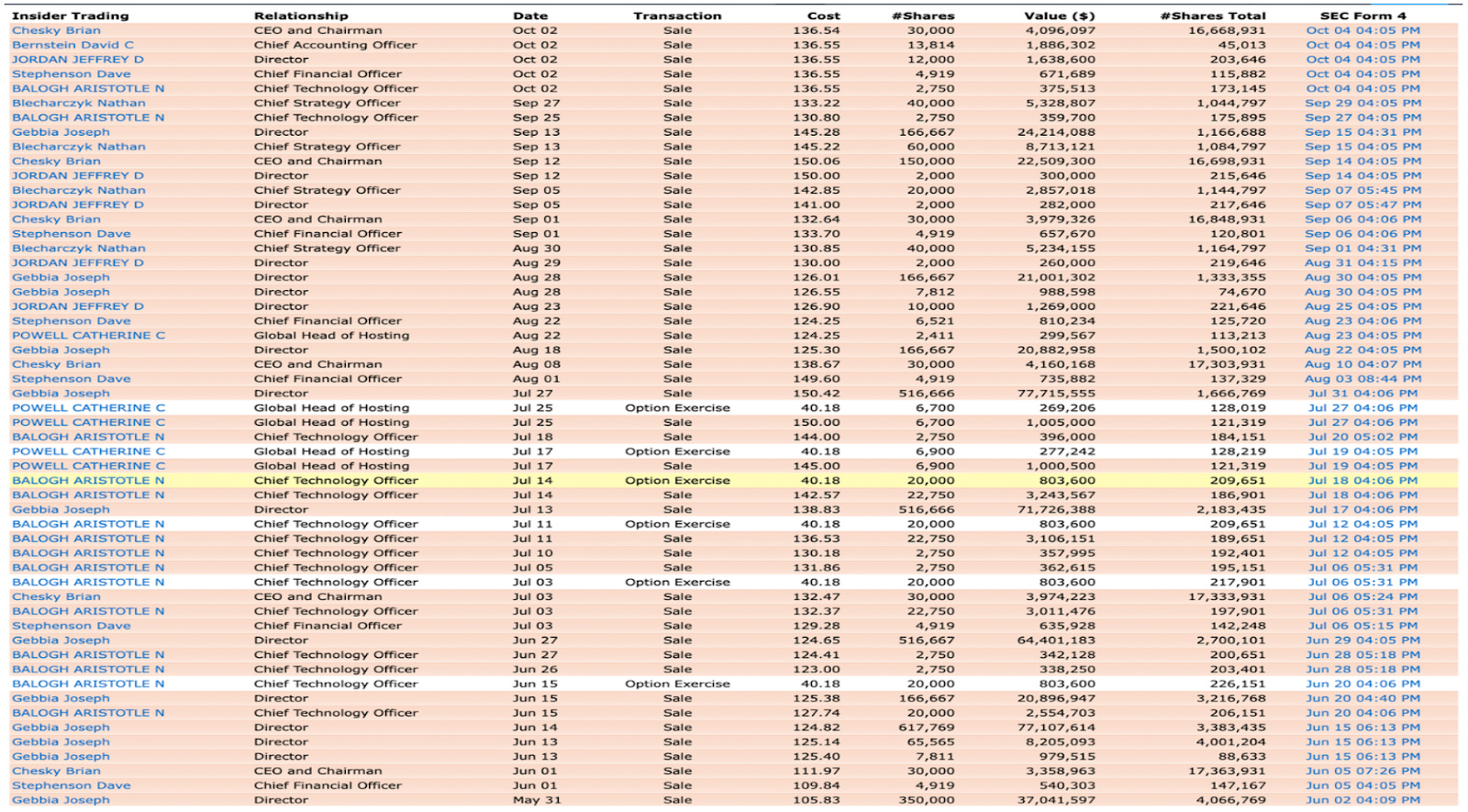

Airbnb remains my favorite short. Valuation is priced for high growth with a Price to Earnings ratio of 37 and a forward PE of 29. ABNB's largest market, New York City, has gone on to ban short term rentals (STR) in the city with few exceptions. Fines for going against their ruling result in fines of up to $5,000 per occurrence. New York City banning STR does not bode well for the future as they are a trailblazer for city regulations. Don’t be surprised if many other cities take a similar stance. With nearly 8% mortgage rates and the highest median income to median housing price ever, ABNB and other short term rental platforms can easily become the scapegoat for unaffordable housing after many hosts levered up at extremely low mortgage rates in order to collect STR properties for “easy income”. “We need to get our house in order,” CEO Chesky said in a recent interview with Bloomberg. The enormous amount of insider sales since the end of May alone doesn’t bode well for the company executives opinion of share price.

I expect potentially a substantial rally from here on pause rhetoric from FED speakers, based on historical parallels. I was expecting to become cautiously bullish for the near term due to historical parallels and as of now am, but that could change if CPI comes in hot this week or additional factions (most notably Iran) enter the conflict in the Middle East. Oil prices may rise this week as conflict in the Middle East causes supply concerns. If Iran gets involved, we can expect to potentially see a major oil price shock to the upside. Absent Iran involvement, oil pricing will likely not be substantially affected.

If the soft landing narrative persists along with a FED pause arriving, historically we can expect to see the market run up as it expects Federal Funds Rate cuts without much slowing in the economy.

Of note, after the jobs report, we saw the first cut being priced in for September of 2024 versus July of 2024 previously. I think it is nearly impossible that the economy, which is used to nearly free cost of capital, can avoid substantial contraction if interest rates stay where they are all the way to September.

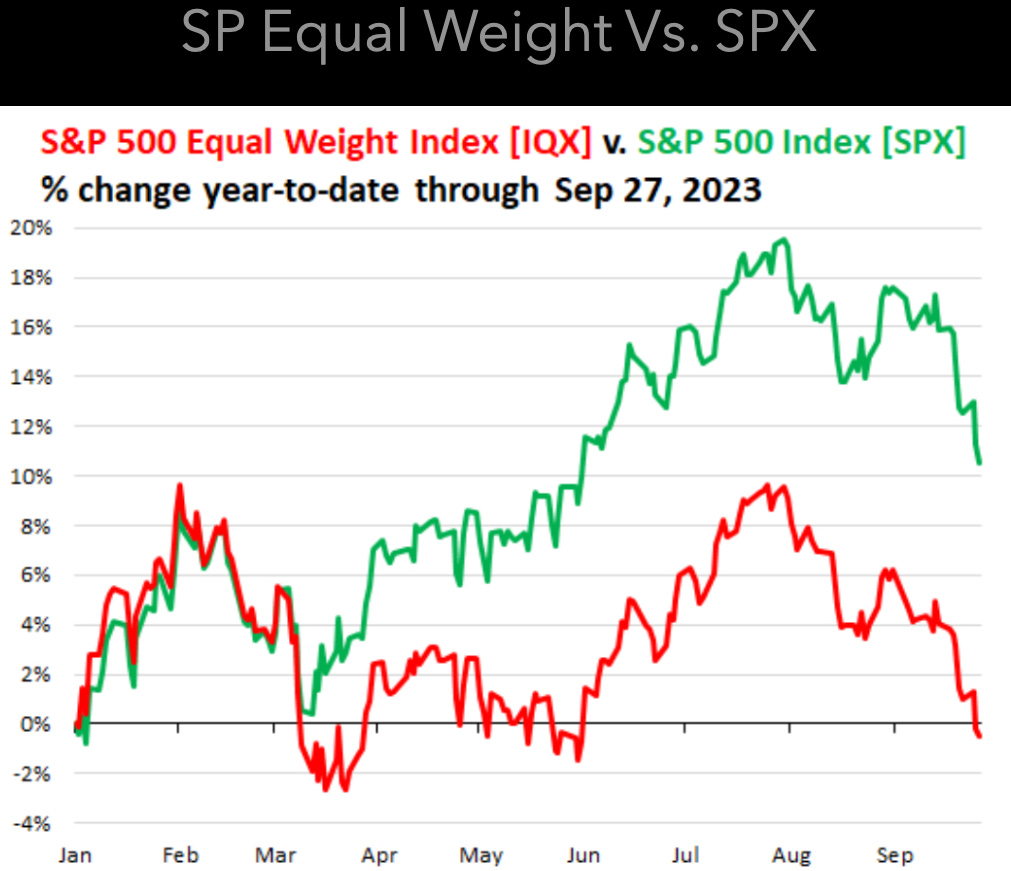

The “ Magnificent 7” trade continues to hold up markets, of which the S&P Equal Weight Index still remains down on the year. From here we likely see continued multiple expansion until economic readings begin to deteriorate and cuts come earlier than forecast, which will not prove to be bullish rate cuts, they will be of the “damage control” nature.

If the 10 year yield and the dollar index DXY remain strong and rising, expect equity prices to remain muted or fall.

Nuclear Winds Changing… For Good? (@SquirtLagurtski, MacroEdge Contributor)

In a recent open forum, Alaska's Lt. Governor Nancy Dahlstrom engaged with members of the Frontiers Group to discuss advancing nuclear energy programs in the state. The Frontiers Project, an Idaho National Laboratory initiative, explores nuclear energy's potential benefits across the U.S. Presently, the project has fostered high-level collaborations with the States of Wyoming, Idaho, and now Alaska, aiming to deploy small modular reactors initially within these states before extending regionally and globally.

These partnerships encompass state leadership, the Idaho National Laboratory (INL), private equity and investment from Evercore, private nuclear industry players like BWX Technologies (BWXT), and construction expertise from L&H Industrial—an Evercore subsidiary. Together, they've embarked on developing a standardized and scalable system for supply chain, industrial production, and operational support, envisioning a national scale-up over time.

BWXT, under the financial auspices of Evercore, constructs the reactors, aiming to establish a comprehensive supply chain standard for reactor design, construction, and installation. Evercore, led by Michael Wandler—known for his manufacturing career at L&H Industries—is pivotal in this venture. BWXT’s representative, Joseph Miller, highlighted the company’s ambitions to foster necessary partnerships for a global expansion of nuclear energy generation.

BWXT is already involved in notable ventures like Terra Power's Natrium reactor project in Kemmerer, WY, and federal projects such as the nuclear propulsion DRACO for the space program and DARPA. Despite past apprehensions towards nuclear energy, stemming from historical disasters, the advent of Small Modular Reactors with enhanced safety features appears to be changing the narrative. The industry witnesses a growing enthusiasm, particularly over the next five years, as stakeholders push for policy and funding partnerships. These aren't isolated projects but indicate deepening collaborations among private firms, investment entities, and the U.S. Federal Government.

Since 2019, substantial funds have been channeled to incentivize sectors like mining and construction and encourage private entities to create a nuclear fuel supply chain. A significant milestone was achieved when Eielson Air Force Base inked a nuclear energy generation contract with Oklo Inc., marking a historic transition towards nuclear-powered military installations. Oklo, a reactor designer utilizing nuclear waste as fuel, through their Aurora Powerhouse and others is supported by investors like OpenAI's Sam Altman, and has spurred renewed investment enthusiasm, demonstrated by a recent $500 million cash influx.

Notable tech magnates like Bill Gates’ Terra Power, and Sam Altman are now intersecting with the nuclear sector, Microsoft even seeking a Small Modular Reactor expert to aid their nuclear transition for data center operations. This move signifies a proactive step towards reducing climate impacts by potentially phasing out diesel generators and minimizing cooling resource demands. Indeed, the fusion of tech and nuclear energy suggests a shift for both industries and the global climate agenda.

Jobs Report and Inflation Leaves Americans Dazed and Confused (@GregCrennan, MacroEdge Contributor)

As legacy media grapples with today's Jobs report and the surge in interest rates, the stark reality is undeniable: America finds itself ensnared in the clutches of a formidable economic challenge – an Inflation Recession. This crisis transcends mere headlines; it's a prevailing issue that demands our

immediate attention. In this edition we embark on a dramatic journey to unearth the root causes and far-reaching consequences of this dire predicament, where the American Dream seems to remain an elusive mirage, rather than a tangible reality that many won’t be able to achieve.

Understanding the Dilemma:

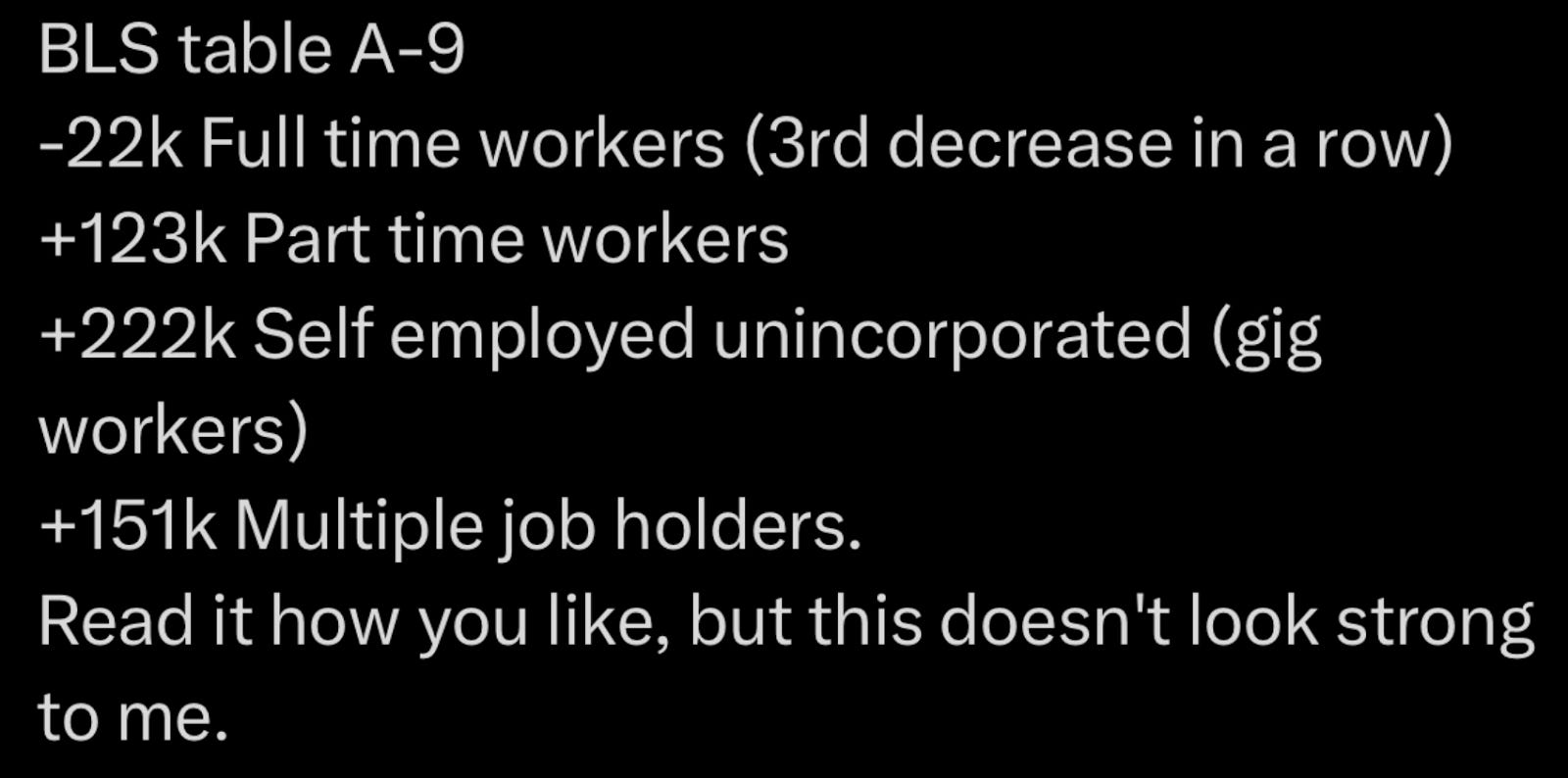

Today's Jobs report seems to be sending conflicting signals. Beneath the surface of the headline numbers lies a stark reality: America has lost 22,000 full-time workers, marking the third consecutive decline. In contrast, the number of Americans taking on part-time jobs has surged by 123,000. Astonishingly, the count of individuals juggling multiple jobs has reached near-monthly record high at 151,000. Why? Simply because many Americans, under their current employment circumstances, can no longer afford the soaring cost of living, courtesy of inflation. Inflation, in essence, is the relentless ascent of prices for goods and services, translating into a decline in the purchasing power of the US dollar over time. Alarmingly high inflation rates have ignited a major cause for concern, casting a shadow over the United States since 2021 and igniting apprehensions about an impending recession born from inflation.

Unearthing the Causes:

The root causes behind the current inflation surge are:

Money Supply: Since 2020, the money supply has seen an astronomical rise of approximately 30%.

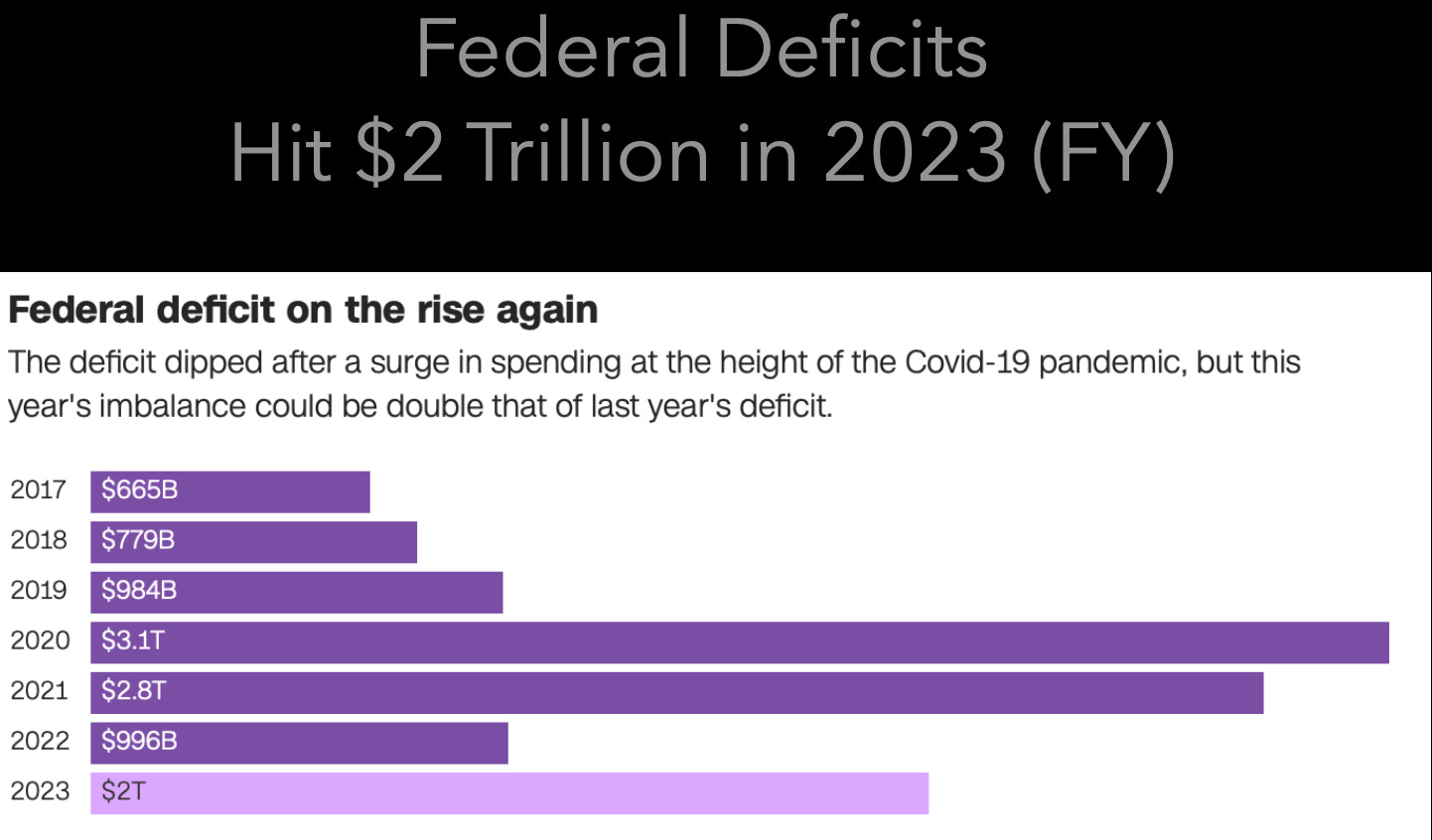

US Deficits: Reduced earnings or unemployment have led to a collapse in US tax receipts, pushing the government into a staggering $2 trillion deficit for FY 2023 the highest ever in a non recession.

Money Velocity: Lagging wages have forced Americans to dip into their savings to meet their expenses, causing a rapid surge in the rate at which money circulates in the economy, resembling a game of hot potato. The saying holds true: "More money chasing fewer goods."

Unveiling the Ramifications:

Purchasing Power Erosion: The relentless price hikes are eroding the purchasing power of consumers, rendering it increasingly difficult to afford essential goods and services.

Uncertainty for Businesses: Rapid inflation has sowed the seeds of uncertainty among businesses, influencing their investment decisions and long-term strategies like the recent strikes.

Interest Rate Alarm: To combat inflation, central banks may resort to raising interest rates, potentially choking economic growth and hiking borrowing costs.

Today's inflation is weaving a complex web across the economy and markets. The trade deficit is dwindling, both in imports and exports. A decline in exports signifies not only a contracting US economy but also dwindling imported consumer goods, including a $1.5 billion decline in cell phones like the iPhone and a $1.8 billion dip in capital goods, including a $700 million plunge in semiconductors. Such decline in both deficits rarely bode well for the economy and companies in those sectors. Consequently, stocks that generally do well in a strong economy when people spend money on leisure consumer good of companies are down significantly in 2023 like Target (-30%), Best Buy (-15%), and Home Depot (-7%) which have faced substantial declines year-to-date. This has intensified price imbalances, misleading investors, and causing the equal-weighted S&P 500 index to be negative in 2023. A clear sign that inflation is gnawing away at earnings and profits for America's top 500 companies. Despite the AI frenzy of the seven Silicon Valley tech companies which combined are up 73% (FNGS) year to date but many of these same companies are still down from their peaks in 2021, while stock indices have fallen over the past two years since 2021.Now, with inflation up by 15%, and interest rates at 5%, future returns are growing riskier by the day.

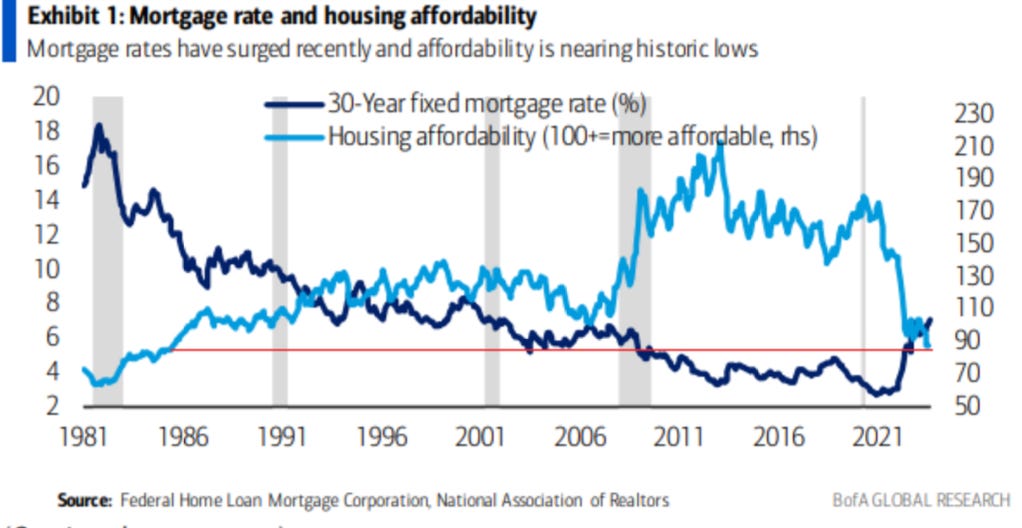

With no signs of slowing down, core inflation remains stubbornly at 4%,

while interest rates continue to surge past 5%. The Federal Reserve's efforts to

tame inflation seem futile, resulting in 30-year mortgage rates hovering at a staggering 8%. Consequently, housing affordability in the United States has plummeted to historic lows. For instance, in 2020, with a monthly budget of $3,000, you could afford a $600,000 home at a 3.5% interest rate. Today, with rates around 8%, that same $3,000 monthly payment buys you a $419,000 home—a precipitous 30% decline in the purchasing power of the American dream.

In conclusion, America finds itself ensnared in an inflation recession, a circumstance where individuals find themselves earning more through raises or multiple jobs in 2023, yet their total income affords them significantly less in goods and services than their lower-income did in 2020. While the government may boast of a robust economy to advance its political agenda, it remains oblivious to the deteriorating quality of life for everyday Americans. As Americans grapple with the paradox of spending more and receiving less, the middle class bears the brunt, while legacy media headlines proclaim a "Blockbuster September Economic Report."

The Economy is Sinking so Follow the Smart Money (@RealJohnGaltFla, Chief Economist)

During the past week, there were two striking television segments which caught my attention regarding the financial markets and the coming collision between higher rates and economic stability.

The first involved a discussion with the hosts of Bloomberg Surveillance where the bond market was the center of attention.

Think about that number highlighted above; if a financial institution purchased a 30 year US Treasury in 2021, they are now down 53% in price. This is an astronomical collapse which will have implications for weaker financial institutions who are sitting on this ticking time bomb and end up in liquidity quicksand. What might that be?

If they are unable to offload MBS (Mortgage Backed Securities) currently stuck on their balance sheets because the Federal Reserve continues to be engaged in Quantitative Tightening, then if said institutions need to raise cash in the public markets they will have to sell more equity (dilution) or those very treasuries at massive losses causing their books to be marked to market at an accelerated pace.

Ergo, selling begets selling.

Marko Kolanovic at JPM has recognized this danger and thus with the bond market in an almost 2008 style collapse has warned we could see a 20% decline in equity prices potentially before year end.

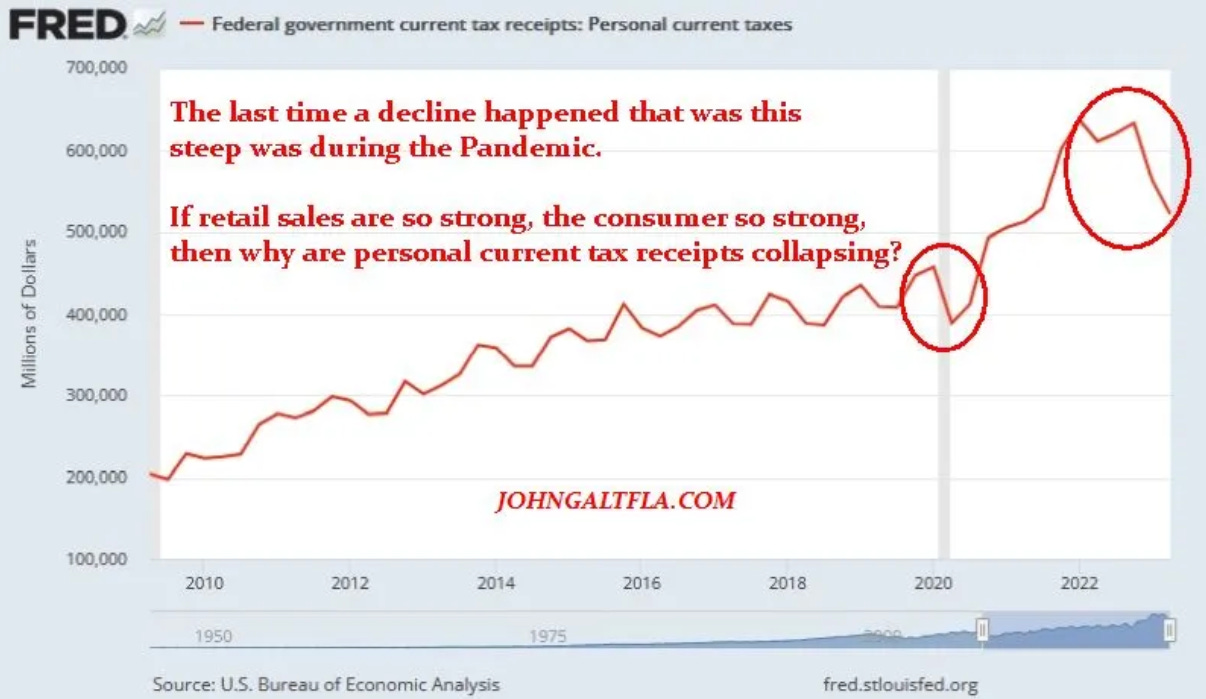

The employment data created the conditions for a low volume short squeeze in equities with poor technical structure and little depth but as the numbers were picked apart, the data produced by the BLS became even more suspect.

Hence, it is time to break down some different but related data points, much more instructive as to the current condition of the American worker and the economy as a whole.

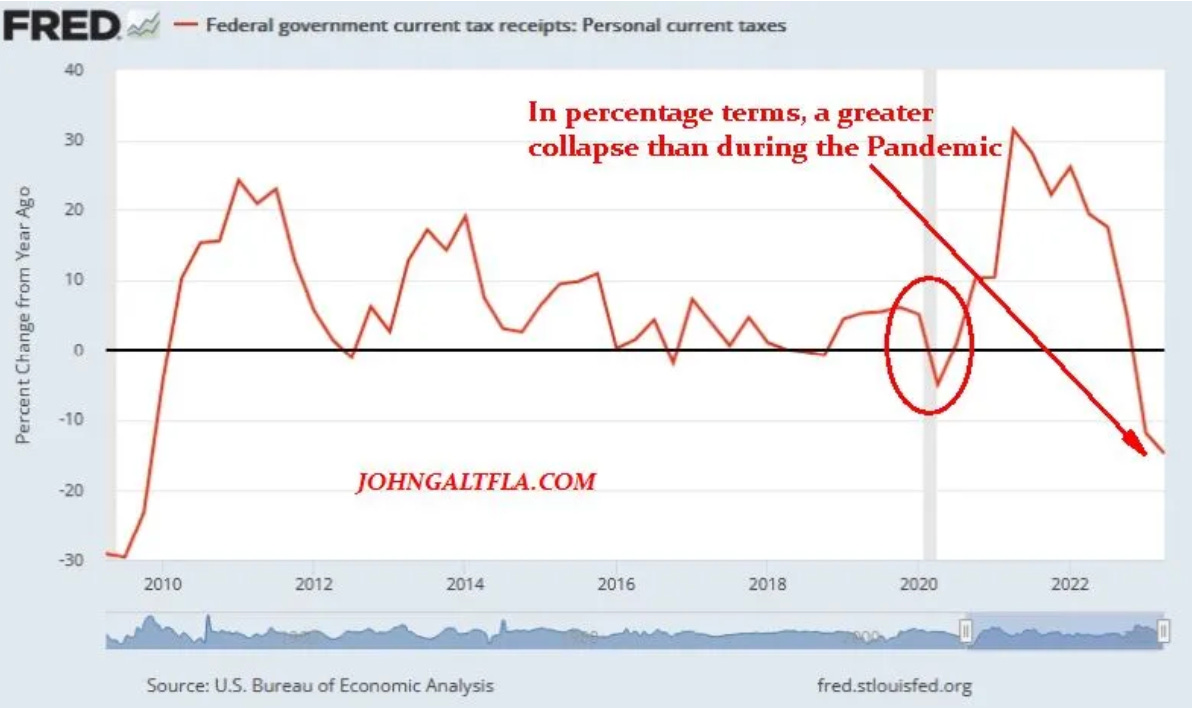

This flies in the face of the claims by the Fed and the administration that wages are stable and strong and not experiencing net deterioration due to inflation. On a percentage basis, the declines are even worse.

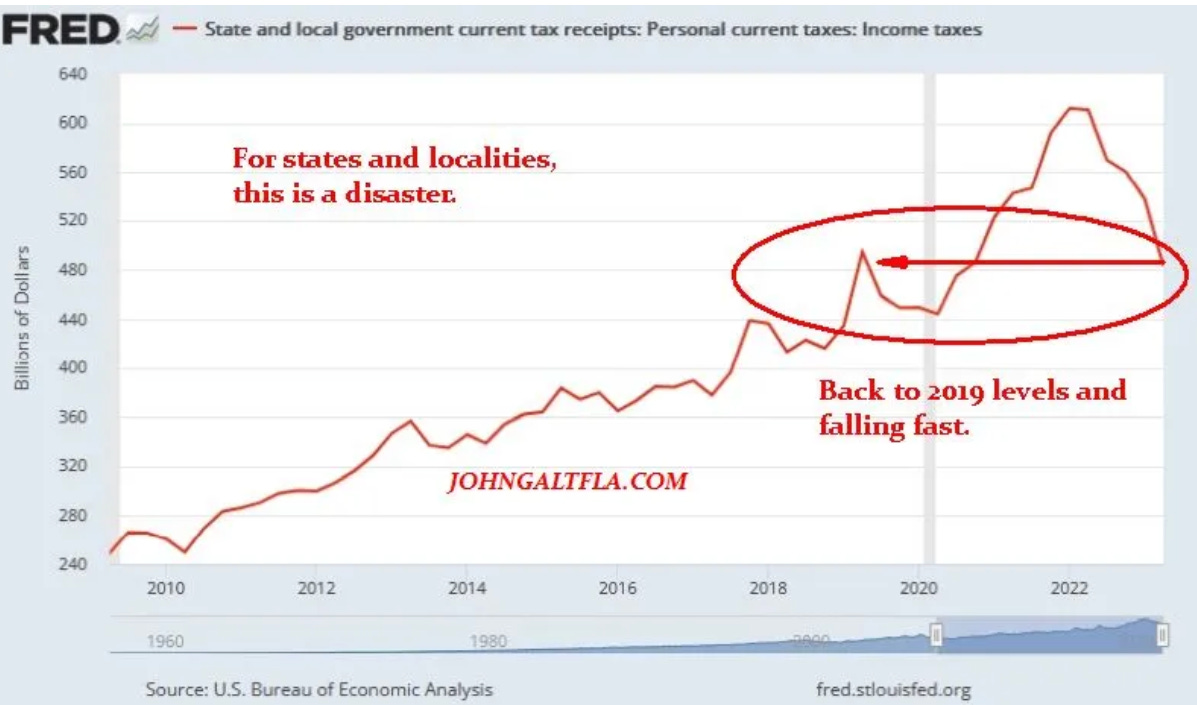

The impacts of these declines is not just on the Federal level, it is going to hit unprepared state and local governments even harder, as the Federal Reserve data is warning about.

Thus despite the “strong” non-farm payrolls report, the underlying well being of the American consumer and their ability to support over 70% of the economy has to be called into question. The ultimate outcome will be a increase in defaults, be it on homes, auto loans, or credit cards unless inflation is tamed (unlikely) or economic growth surges with wages to offset the impact of stubbornly higher rates of inflation.

These are signs of an economy falling into recession, not recovering from a pandemic and continuing strong sustainable growth. The layoff data does not lie and it is beginning to indicate the same headwinds.

Watch the smart money this week, aka, the bond market.

The bond traders know what is coming and how the flood of issuance by local, state, and the Federal government into a stagflationary environment will impact rates over the long term.