10/15 Weekly Report - 'A Dotcom Redux, Nevada Housing Review, Earnings Season, Inflation Data, and More'

In this weekly report - Don, Six, Joe, Greg, and John tackle everything from the evolving technology employment data in California, to the emerging nuclear market, and more.

10/15 MacroEdge Weekly Report

@DonMiami3, MacroEdge Chief Economist

@SixFinance, MacroEdge Head of Research

@SquirtLagurtski, MacroEdge Contributor

@GregCrennan, MacroEdge Contributor

@RealJohnGaltFLA, MacroEdge Contributor

Weekly Data Update and Report on Nevada/Bay Area (@DonMiami3, Chief Economist)

Another Sunday, another weekly report.

I've just returned from a productive trip to Nevada, and there's a treasure trove of data waiting to be analyzed. Nevada presented some intriguing data points, particularly around employment and housing that warrant our attention. Drawing parallels, the Bay Area's current economic climate seems to echo the Dotcom era in some ways. Today, we'll unpack these observations, ensuring we stay grounded in the facts. Let's explore together. I also want to point out that Ascend Pre-Access is available coming November 5th for those interested in the professional research reports for you or your organization. You can signup for an account at https://www.macroedge.net/get-ascend. The Data Dashboard will also be available on that day as well.

I was able to start the trip off winning the week’s worth of fantastic dining experiences/Vegas food on a blackjack table - so that is never a bad thing. Like most gamblers, many market gamblers don’t know how to quit while they’re ahead… which is something I took advantage of after leaving the table in 5 minutes. In Las Vegas particularly - I was not surprised at the continued robustness of the economy… At the time of my visit last week there were 3 overlapping conventions and hotel prices were wild (add on a Pink concert, a Raiders game, and the Sphere) and it was probably the busiest I’ve seen it over the many times I’ve been dating back to the mid-2000s. Airport was also jamming. While these are all continued positive facts for Nevada and the employment situation there - I do expect the state to begin seeing a slowdown on the labor front over the next 2 quarters - particularly when consumer spending actually begins to drop beyond the margins. While the housing market remains largely frozen as it has in many other cities - prices have come down a bit off the top. Many of the new home communities I looked at were offering generous comps/buydowns to get inventory off of their hands with mortgage rates at 30-year highs. Gaming revenue data remains strong in the state but inflation-adjusted is still below the crazy peaks seen in the 2006-07 years (highlighted in a previous write-up).

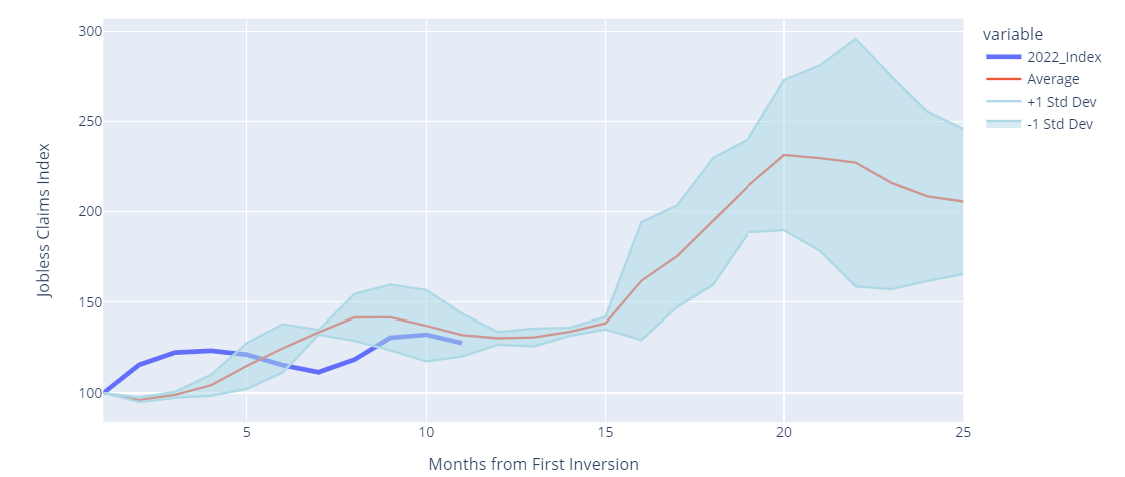

Jumping back to the Nevada data - we have the final continuing jobless claims figure from the state through the end of September. The current cycle is progressing right within the average of the 3 previous ‘modern cycles’ and following month 16 of inversion we should begin to see claims take the turn upwards unless the lag is longer this cycle - or the Fed achieves the ‘soft landing’ (unlikely).

Employment growth in the state continues to look strong - driven in the hospitality/lesiure sectors, manufacturing, and construction - although it’s very important to remember the very long lag seen in Nevada in regards to rate hikes and labor weakening of the labor market. Giving the housing market weakness that I observed and have been keeping an eye on in the state - residential construction employment slows down over the next 2-3 quarters - especially on the multifamily side. Even with the population growth in the state - the levels of multifamily construction are at wildly unsustainable levels and I think a weakening labor market is likely to bring up inventory on the single-family side of the equation. Turning to Reno - I think this is where you have more exposure to the coming slowdown. Job growth rebounded in August after turning negative, but the city is still heavily anchored to leisure and hospitality which likely sees a larger slowdown through 2024. While the state’s economy remains strong and the roulette wheel is spinning - I think 2024 may be a year where the Nevada economy finds itself landing on the red and watching continuing claims data through the next 2 quarters will give us a very good picture on how we can expect the Silver State’s economy to perform over the next year. I do not believe that this will be a 2008 redux for Nevada given the population growth in the state and diversification of employment across various sectors. In my report next week - I will go into more of the housing data on a city/city basis so you all have a better idea of what I was able to get my eyes on and what’s occurring on the residential real estate side of things there.

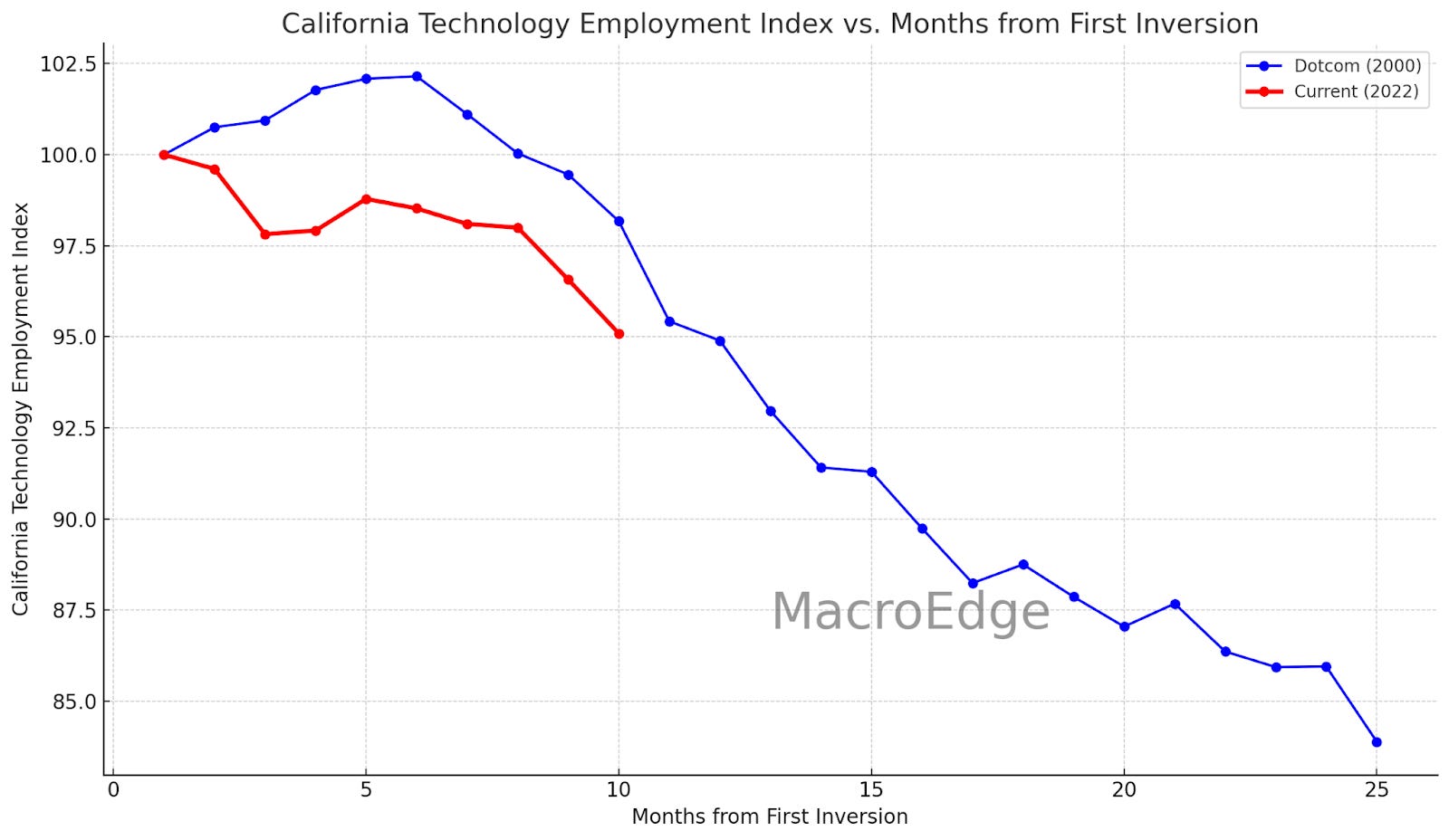

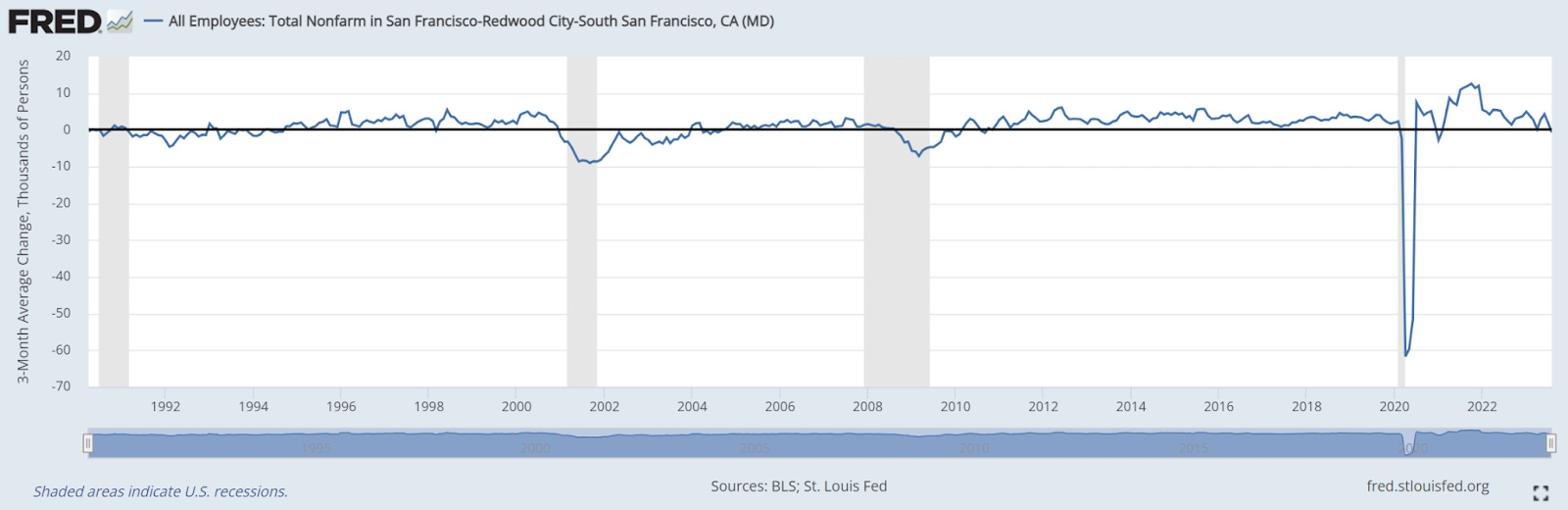

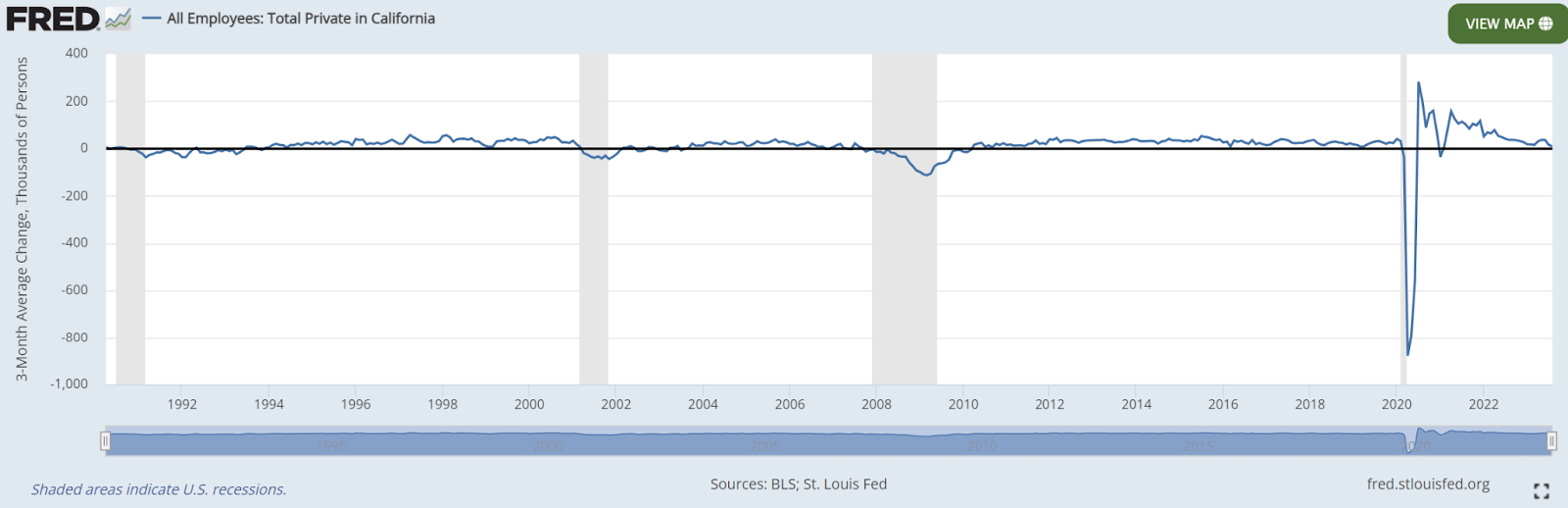

Now turning our attention to the Bay Area and California - I want to draw some similarities to the Dotcom economy, particularly on the tech employment front and aggregate employment front. Looking first at aggregate tech employment in the state of California - things are looking very similar to 2000 thus far, in fact it’s slightly worse in % terms. This has caused employment growth in some areas of the state (notably San Francisco) to actually go negative [second graph below].

What we need to lookout for is continued contraction on the employment front in the Bay Area in an ‘echo of the Dotcom era’. Growth in leisure in hospitality is slowing considerably in the Golden State and other leading/cylical sectors - as is the total employment picture:

California may be the leader this cycle given its poor demographics, outward movement, and terrible environment for businesses. Hope this was some useful data on where things are at in the Silver and Golden State’s respectively - and let’s continue to lookout for a ‘Dotcom redux’ given equity valuations where they’re at and the number of unprofitable companies still occupying the markets today. I have a feeling we may be seeing the arrival of the redux in the next two quarters.

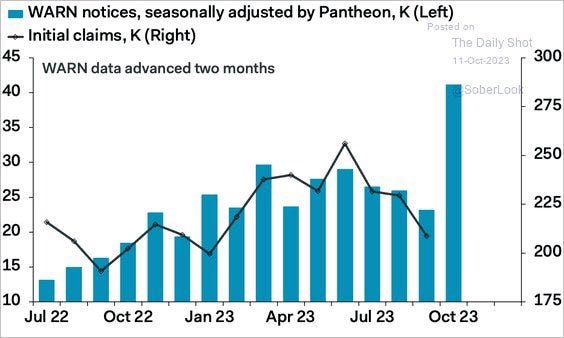

Take a look at the WARN notices as well… this warrants caution ahead on the labor market:

Enjoy the below reads from the team and make sure to check out Ascend if interested (MacroEdge.net).

See you all next weekend.

DJ

Weekly Market Review (@SixFinance, MacroEdge Head of Research)

Large bank earnings came in with beats across the board, showing strength in the banking sector among GSIBs. KRE regional banking etf continues to show weakness following several regional bank collapses earlier this year. Big Bank ETF (BIGB) to Regional Banking ETF (KRE) relationship shown below.

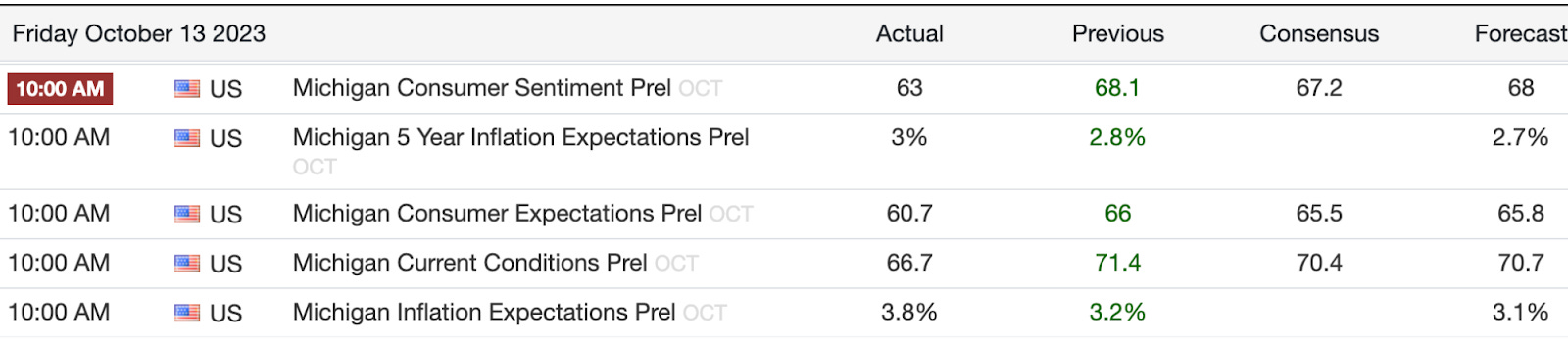

CPI and PPI inflation measures both came in hotter than expected. The FED is clearly not done with their war on inflation. Michigan surveys also showed poor results as consumer sentiment is weakening and forward expectations for inflation came in significantly above expectation.

The situation in the Middle East has continued to deteriorate with Israel air striking two of Syrias’ largest airports and Iran begins to verbally show signs of potential involvement. This is a situation to watch closely.

The UAW autoworkers’ strike continues to stalemate as on Friday the UAW told the Ford CEO to “get the big checkbook.” Ford is also a company we are monitoring that is laying off workers right now. The strike may not go the way the UAW hopes.

Oil broke out monday and then declined through the week before exploding higher on Friday in anticipation of Israeli' ground war into Gaza. The volatility index VIX also finally broke out to the upside on Friday in what appeared to be a risk off day for markets. Bloated tech names fell in outsized fashion relative to the market as a hole.

A weak 30 year auction on Thursday caused yields to explode higher intraday before declining through the end of the week as a flight to safety bid in US Treasuries ensued before a weekend of market risk in the Middle East. Popular retail bond ETF TLT saw enormous volume last week, with a slew of risk mounting. Interestingly, the dollar index DXY continued to show strength even as bond yields fell, cementing the flight into the relative safety of the United States dollar and debt.

Fed speakers all week alluded to rate hikes being done, and I believe we will not see another. WARN notices (2 month advance notice of layoffs by companies with at least 100 employees) have skyrocketed higher this month, to nearly 50% higher than the highest month since the tightening cycle began, and it is only the 15th of the month.

From here, I believe the cumulative tightening of all rate hikes begins to take hold on the economy and markets, and quickly. The “Magnificent 7” stocks will begin to underperform, housing prices follow the downtrend expressed in mortgage demand.

There are two options that lie ahead of us.

Rate hikes crash the economy and we see a hard landing, crushing asset prices.

The economy somehow manages to hold on and the FED then sticks to the dot plot,which stymies any and all growth, which eliminates further growth in asset prices.

I believe Option 1 is exponentially more likely than Option 2, however neither are bullish for asset prices at the moment. The asset bubble that we are currently in, which Stanley Druckenmiller says is the greatest asset bubble he has ever seen, is rooted in Treasuries. Treasuries have taken their beating. Now with interest rates very high, other asset prices will follow suit.

For the Equity Markets, once the SPX loses its’ extended bear market rally(and yes I do still believe thats what we have seen this year, a prolonged bear market rally spurred on AI hype following Chat GPT release) trend, things could get ugly in a hurry. The nasdaq 100 continues to trade at nearly 30 times earnings, a ridiculous valuation given interest rates and lending conditions.

A Nuclear Update (@SquirtLagurtski, MacroEdge Contributor)

The United States has recognized a need to make up lost ground in the race for clean energy, it’s not solar or wind generation. The Department of Energy has been funding advancements in nuclear energy since 2019 and the U.S has been incentivizing nuclear projects through some of the largest tax credits to date. Nuclear energy can make up for the shortcomings of wind/solar and is now being deployed in multiple states from Alaska to Michigan with projects being approved and designed across the nation, the U.S is already a global leader in nuclear energy and actively seeks to widen that lead through cooperation with U.S based companies in the creation and deployment of a supply chain for raw materials and mining, reactor design and deployment, back end support and operations, and emergency response and safety. A renewed push for carbon neutral energy has led to major advancements in the design of nuclear reactors with breakthroughs being achieved in Small Modular Reactors (SMR) by multiple U.S based companies such as Oklo, Terra Power, Nuscale Energy, BWX Technologies, and others.

Since the Chernobyl incident in Ukraine back in 1986 fear of nuclear energy had been key in the underdevelopment of proper, and safe nuclear energy generation. The world was introduced to the power of nuclear fission in the form of explosives during World War II with the bombing of Hiroshima, and Nagasaki in 1945. After the bombs were dropped and the damage assessed there were overwhelming reactions on the world stage and calls for the technology to never be used again, rightfully so. The sheer magnitude of the explosions and their fallout haunted world leaders and created a deep distrust in any use of nuclear fission to generate electricity. The Chernobyl disaster in 1986 only worsened the public view on nuclear energy and back in 1979 the three-mile island incident in Pennsylvania seemed to be the final nail in the coffin for potential usage of nuclear technologies as a form of energy generation.

The concept of Small Modular Reactors has been around since the 1950’s and have largely gone underdeveloped for decades due to multiple factors, fear of the technology is the largest factor but its important to realize the expense of the development, its capabilities for energy generation, regulatory blockades are among the other limitations faced in their design and potential development, those hurdles have largely been removed through years of costly research and meticulous planning by private and government entities alike and breakthroughs in the technology have only recently been achieved, in the 1990’s the Idaho National Laboratory began research and development in SMR’s without the U.S government support and currently the INL is currently on the forefront of the technology still with partnerships throughout the growing industry, they are largely the most influential resource in the space. Since 2011 the International Atomic Energy Agency has been providing updates on the development of SMR’s and has been an important resource as well. A major development came in 2018 when the Nuclear Regulatory Commission accepted a design certification application from Nuscale Energy, allowing the further development of SMR’s, and in August 2020 Nuscale’s design was put into final technical review and subsequently certified in July of 2022 marking another major milestone for the technology, and the first ever certification in the U.S for the use of a SMR.

Back in 2019 the Department of Energy created the advanced SMR R&D program, which supports the research and development of the technology from design to deployment and allocated over $300 million, the funding included the R&D, testing, education and training, with over 40 state level universities participating in the program and have made significant progress on all levels, the program not only focuses on domestic applications but is also engaged with U.S strategic and economic partners across the globe. Those partnerships include SMR development for Romania’s ongoing nuclear energy development, along with Ukraine, and Japan.

Nuclear energy checks multiple boxes in the ongoing climate agenda for the U.S, wind and solar energy have been marketed heavily to consumers as a cost saving, carbon neutral source for clean energy but have also proven to be less effective than previously stated. The amount of infrastructure required, cost of deployment, consistency, and development have all shaken trust in their capabilities and for lack of a better description they’re a fallacy. Both solar and wind solutions are not long term, and they’re simply too expensive to maintain realistically at scale. Acres upon acres of quality farming land in southwest Michigan as an example are currently being littered with solar panels stretching for miles and costing billions of taxpayer funding to provide less consistent and reliable energy. Nuclear energy, and SMR’s have the potential to bring exponentially greater energy density per kWh, use a fraction of the land, are completely self-containing (meaning if they fail they do not need human interaction to shut down), have a much longer lifespan (30-80 years before fuel is needed), do not have negative effects on the habitat of local animal life, and most importantly they create consistent, stable, carbon free, and energy dense solutions in every environment including during adverse climate conditions. The Alaskan Powerhouse reactor which has been approved for use at Eilson Air Force Base provided in a partnership with Oklo was chose based on the needs of the base during sever inclement weather given the base’s location and mission critical operation for U.S national security. Oklo has developed an SMR which uses nuclear waste (spent nuclear fuel) as fuel for the reactor, which is the first of its kind, making the reactor completely carbon neutral while also utilizing waste as a fuel for energy generation. This is one example of the exponentially greater capabilities of nuclear energy over wind/solar counterparts.

Note: Oklo was recently backed by Sam Altman, creator of OpenAI and will be taken public through ALtmans SPAC. They received $500 million in fresh funding through the deal.

Centrus Energy has begun to enrich uranium into fuel for nuclear reactor projects across the nation and stands as the first to do so since 1954 in support of the Department of Energy’s growing partnerships with private companies to develop a supply chain based in the U.S which will support its nuclear portfolio. Centrus has also partnered with Oklo, Terra Power to supply and support operations for Terra’s Natrium project in Wyoming, X energy to develop and construct a fuel fabrication facility, Radiant Industries, Terrestrial Energy USA, and others in support of the Department of Energy’s supply chain development for energy security as the nation seeks to continue to lead the global nuclear clean energy market, and eliminate the need for Russian uranium and fuel which currently supplies 90% of the nations needed fuels.

The nuclear energy arm within the energy sector continues to branch out independently from the pack and has in the last five years began to grow exponentially with more private investment, government policy changes, state and local investment, and engagement within communities also beginning to accelerate. There have been major developments in the technology and safety of nuclear energy, the capabilities of the reactors to provide cheaper and more reliable energy solutions for consumers, the public opinion of nuclear as a clean energy source, and the motivation of investors who seek to obtain exposure to the energy sector to invest in a market with long term potential. By no means does this imply there aren’t setbacks, there are always risks when investing into an emerging subcategory of a market sector, but as with gold, equities, treasuries, there is a risk to reward which has been starting to lean more equally in the last years that hasn’t occurred in decades for nuclear energy. The value created by the companies which are currently seeking partnerships between the Department of Energy, private investment, and others in the space has steadily accelerated and is currently in the demonstration phase. The larger picture being painted in my opinion and backed by the research I continue to do shows the U.S looking to partner and build an entire new market within the energy sector based on the capabilities of current U.S based nuclear energy providers, raw material miners/producers, industrial leaders, private investment firms, and with global partners from the ground up based on the regulatory achievements, policy changes, tax and investment incentives, and cooperation with state and local municipalities, and will surpass the shortcomings of the solar/wind applications which have floundered over the last decade and continue to prove insufficient for adequate carbon reductions and energy production/stability.

Amidst Unyielding Inflation (@GregCrennan, MacroEdge Contributor)

In the face of adversity and economic challenges, today's inflation report have brought more unsettling news for Americans and investors. It seems that we're all echoing the timeless lyrics of Bon Jovi's anthem, "Livin' on a Prayer,” with hopes that inflation returns to the past decade normal and grapple with a harsh economic reality that continues to test our resilience.

A Misleading Year of Expectations

Over the past year, the government and legacy media assured us that a soft landing and a return to normal were on the horizon. However, today's report on price increases shows a stark contrast to that promise. Many of us are down on our luck, as investments fail to help us get ahead. The bond market has experienced a significant crash the worst in US history, with interest rates hovering around 5%. As a result, Americans are just barely getting by, with wages struggling to keep up with inflation, forcing many to work multiple jobs not just to achieve their dreams but simply to stay afloat.

Inflation: The Unrelenting Foe

The relentless foe behind this uphill battle is none other than massive government deficit spending. In the past three years, the government has increased the money supply by a staggering 30%, leading to an equivalent loss in the purchasing power of the dollar since 2020. The consequences are clear, and they weigh heavily on the average American's shoulders.

The Hard Truth: A Shrinking Dollar

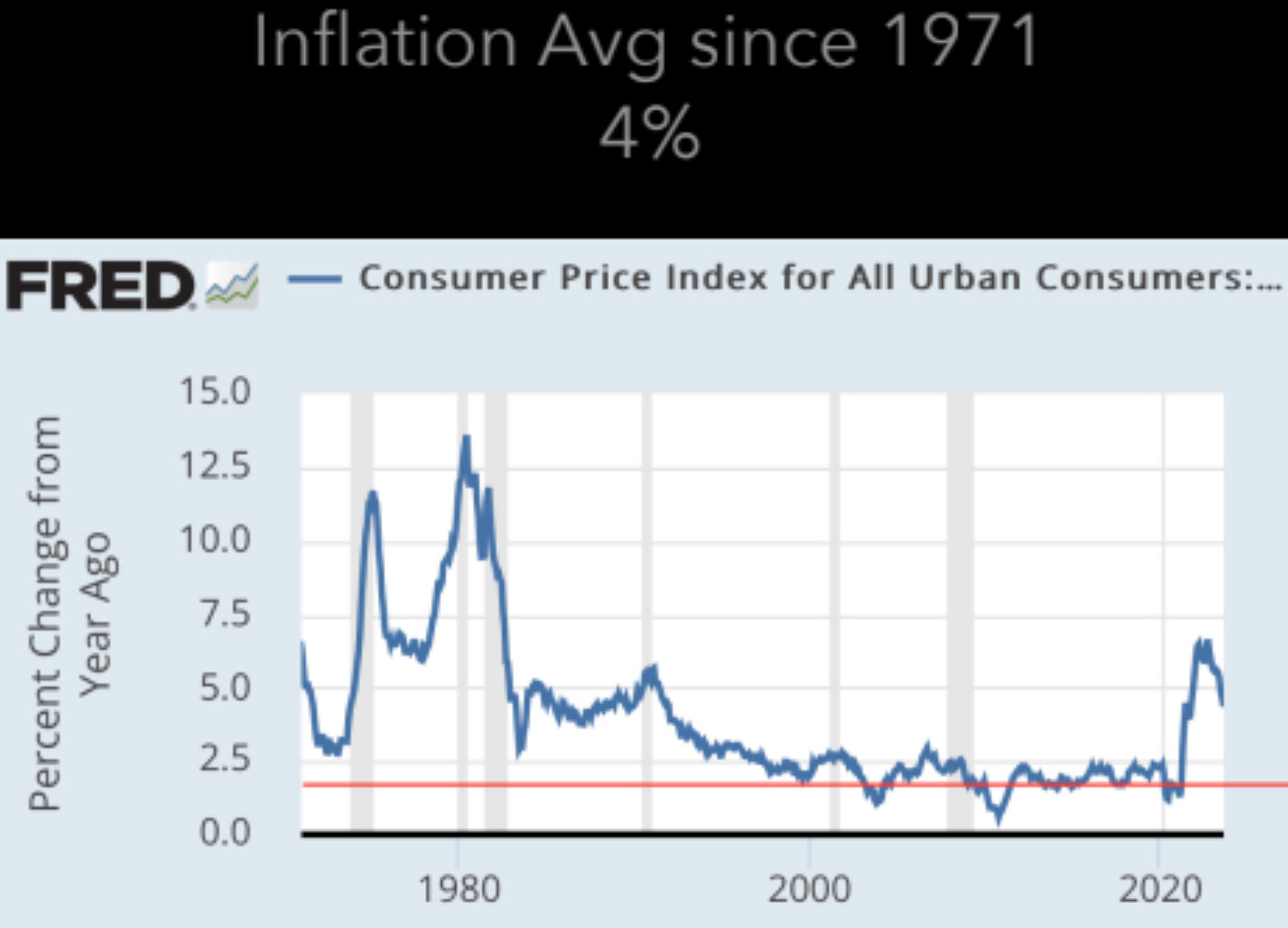

To put this in perspective, if your salary was $100,000 in 2019, you'd need to earn $130,000 today just to maintain the same standard of living. Unfortunately, many Americans have not seen such increases in their income. With no signs of inflation slowing down below 4%, if this trend continues, in just another 10 years, by 2033, you'll need an annual income of $200,000 to purchase the same goods and services you enjoyed with a $100,000 salary in 2019.

This scenario is the most likely one as it is based on historical annual inflation averages since 1971 at 4%. But this will just be keeping up with the cost of living not surpassing it, especially considering higher tax brackets, which could result in less take-home pay relative to the rising costs of goods. It's a challenging reality that many are starting to recognize and now are taking on a more profile stance or fight. As Bon Jovi aptly sang, "Oh, we've gotta hold on, ready or not, you live for the fight when that's all that you've got."

A Glimpse at Today's Inflation Data

The Coastal Journal this week isn’t breaking down the price increase categories since the increases are so drastic now that everyday Americans are witnessing these price increases in their day-to-day expenses, from home utility bills to the gas pump and the grocery store. The inflation problem can be solved, but the real question is when the government will take action to address it by reducing the deficit, raising taxes, and reduce government spending? Today, we're all living on a prayer that this inflation can be tamed, maybe a change in 2024 can make that happen, but until then, everyone right now is echoing the sentiments of Bon Jovi's timeless refrain:

“Oh, we’ve gotta hold on, ready or not

You live for the fight when that’s all that you’ve got

Were half way there Oh, Living on a Prayer

Take my hand and we’ll make it, I swear

Whoa OH, Livin on a Prayer”

The Cumulative Inflation Dilemma (@RealJohnGaltFla, MacroEdge Contributor)

The media and the Fed seem to have declared victory over inflation this week. If this is your first experience with inflationary periods like this, then odds are you are not as old as I am.

If one thinks that the inflationary cycle has peaked, then you were not around for what happened to the Federal Reserve in 1978. The idea was that the rate of inflation was starting to fade as oil prices and food prices declined. There were still a great deal of labor unrest, but in the end the rate of change had subsided.

Fast forward to September of 2023. The media promotes the theory that although inflation is higher than the Fed’s target it is not that bad. Here is you mainstream media headline to highlight that idea just three days ago from CBS News:

U.S. inflation moderated in September, but is still too hot for Fed

Moderated?

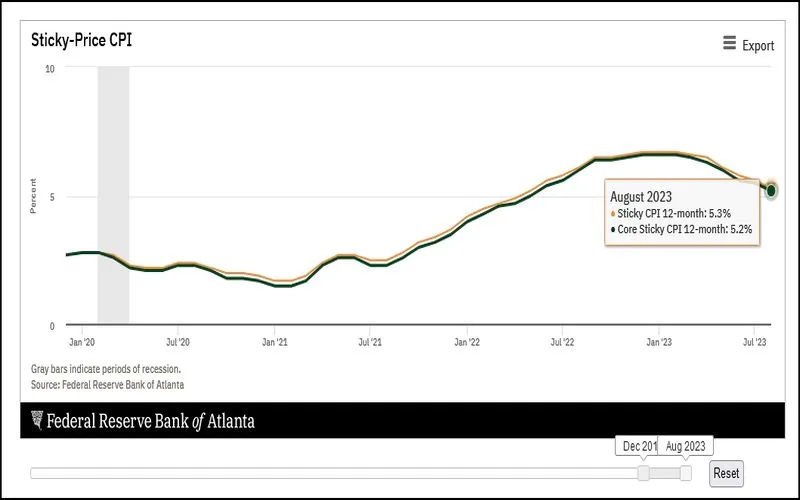

Here is the Atlanta Federal Reserve’s Sticky CPI tracking for September with data back to just before the Pandemic:

While the trend is down, the cumulative impacts of this recent inflationary episode is still being felt by the American consumer. If one uses the somewhat debatable data collection techniques and reporting of the Bureau of Labor Statistics, it portrays a far different story. Even if the inflation data is far short of reality.

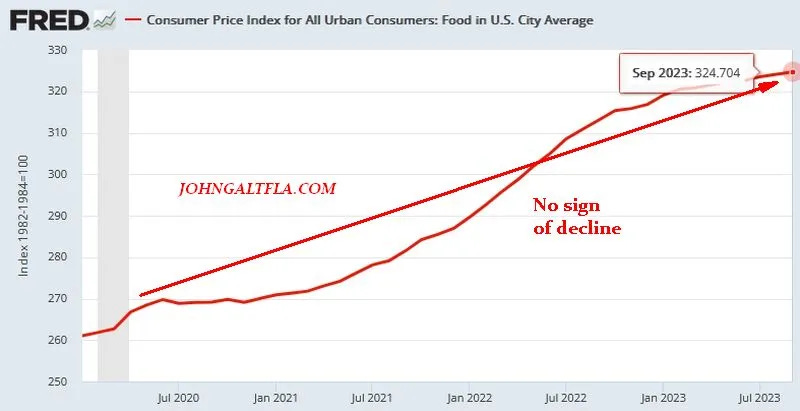

For example, one of the most expensive items the media economic cheerleaders wants everyone to ignore is the cost of food. Unfortunately for them most Americans still go grocery shopping and the immediate impact of higher food prices on the consumer. The chart below is based on the BLS’s own indexing to 1982 dollars and illustrates the sustained, persistent cost of cumulative inflationary pressure:

Thus the idea that “prices are coming down” is a relative or political concept, not an economic reality.

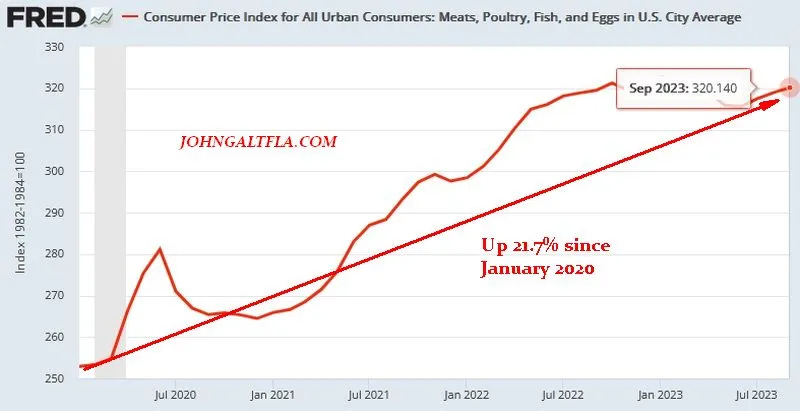

Breaking it down into several expense categories consumers deal with provides a much clearer picture of the pressure put on the average American citizen.

For example, the basic protein complex is not displaying a “moderating” picture for people who wish to eat:

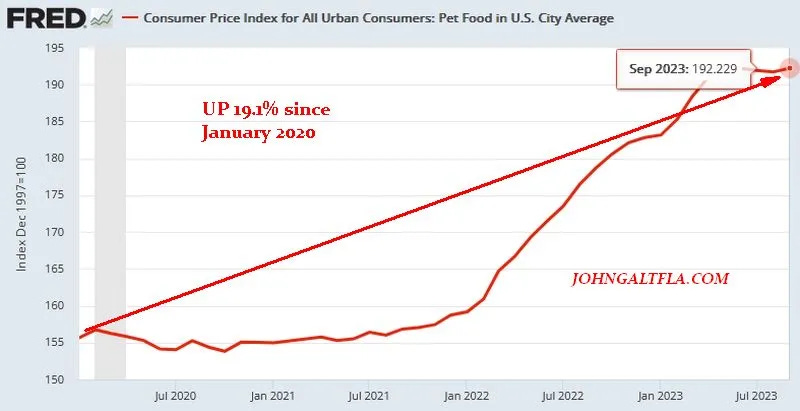

It’s not much better for pets either:

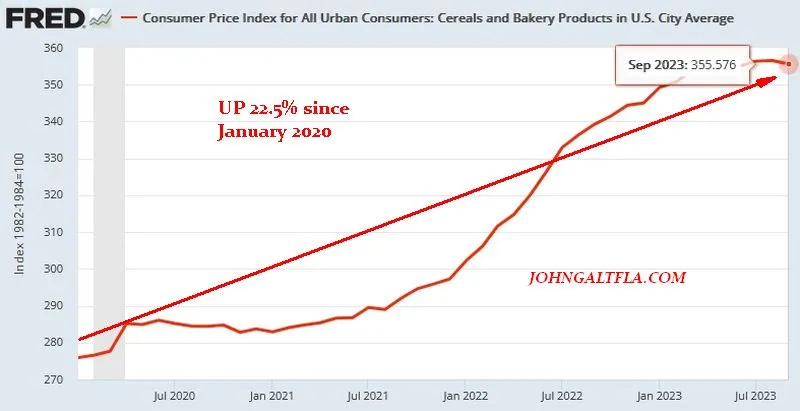

Thankfully, if one believes the BLS bureaucrats, people do not eat bread, cereals or other grain based foods, right?

The heck with eating. Nobody really cares about that because everyone said the inflation data is only important if one excludes food and energy.

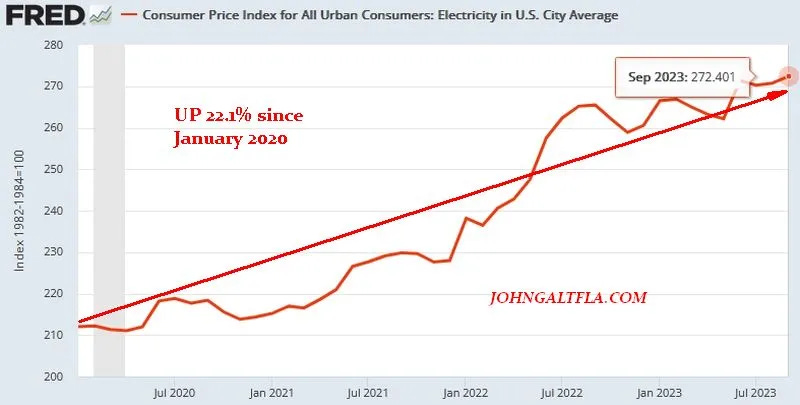

Speaking of energy:

Unfortunately people ignore the constant piling on of inflationary pressures on the citizens and still attempt to focus on the “feel good” aspects of the data. The “hey, eggs came down last month” media propaganda is useless when one’s homeowner insurance doubles, auto insurance shoots up 25%, or medical insurance is slated to be increased by 20% or more.

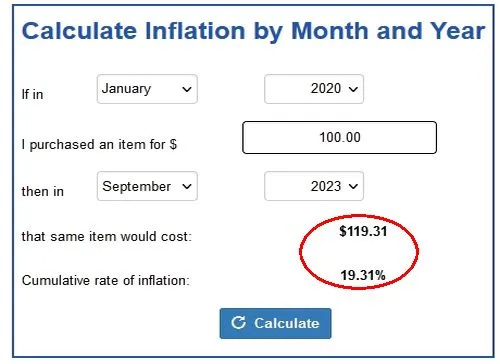

The truth is cumulative inflation over the decades has destroyed any wage or salary increases for more than 80% of the population. Just since the Pandemic era, it was devastating for the average family as the Inflation Calculator demonstrates using the BLS website.

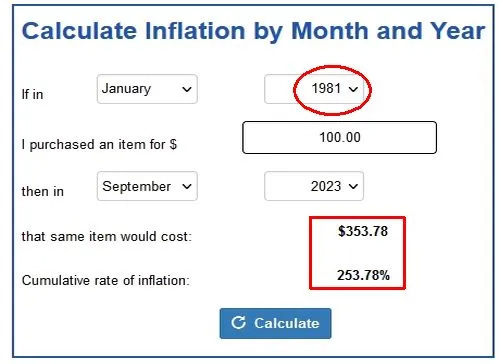

If your wages only increased by $10 per week since then but inflation is up 19.31% you’re falling further behind. But wait until you get to be old like some of us to see the real problem. Since the last inflationary episode in 1981, the US dollar’s purchasing power has declined by a frightening pace.

This is not sustainable however it has to be. The US government can not allow for a deflationary episode to reduce prices for homes, cars, or consumer goods.

Because then and only then would the risk of default on our national debt become a reality. Hence, buckle up for even more inflation at higher and faster rates for longer in the years to come.