10/12 Weekly Macro Note: Cheers from the Casino, Holiday Releveraging, Rest of October, the MOAB, Cracks in Gig Employment

In this Weekly Macro Note, we digest the Friday deleveraging & Sunday morning TACO, talk about the animal spirits among retail investors, highlight critical data this week, and much more. #MacroEdge

(@DonMiami3, Chief Economist)

Good Sunday evening MacroEdge Readers & Community,

The title of our article this evening is ‘cheers from the casino’ - which are audible tonight after the President greatly softened the tariff tone on China as expected. The 100% tariff threat is now a tool, but it was greatly blunted today after VP Vance came out & stated that Trump was only using it as a negotiating tactic. Given what we’ve discussed in our previous reports over the last week - including in the Institutional Research report for October - the bubble created from April has become not only a systemic one, it’s a national security risk. With nearly 65% of American households involved in active speculating in financial markets today, including the cryptocurrency crowd, Friday was only a minor preview of how quickly left-tail risk can strike.

Previews of these vulnerabilities are not a timing instrument, but provide valuable signal in the noise of the absolute casino-like environment that markets continue to face (note retail inflow data from 1W September to 1W October being the largest ever at almost $100bn in inflows on a rolling basis). The politburo has created the ‘MOAB’ and the phones are ringing louder every instance a deep is even seen in equity (and now crypto markets…)... how’s that for pro-free markets?

Other noteworthy posts from Trump today included a direct shot at the homebuilders, and they may be next in the crosshairs for some kind of government rollup / absorption bailout engagement with how weak conditions are for them. Think Intel-like, but money after the fact, given that Intel received ~$10bn in taxpayer funds from the CHIPS Act under the previous president. Friday once again revealed that the macro issues are much deeper than just tariff Truth Social posts, but window dressing will once again keep the masses distracted from the ‘under the hood’ problems permeating private credit, consumer lending, regional & community banks, and more broadly - the employment market. Just the anecdotes alone this weekend on the speculation & retail behavior continue to have me thinking we’re in an environment only comparable to the late 80s bubble environment and pre-1929 behavior. The reality of this egg is it’s going to take a lot more than a single risk-off day to dismantle the spirits of a new-era of gamblers ready to fire capital at every first sign of risk off with the fiscal put being ready to step in on a moment’s notice & keep the party going.

RE: Institutional Research - we will have a full update piece out tomorrow, and are awaiting the domain connection for the alpha dashboard. We now have the Institutional Research Substack live & secured, which can be found at MacroEdgeInstitutionalResearch.substack.com (an absolute keyboard full, but Substack doesn’t allow for Sub-sub domains)…

Don’t have MacroEdge Ozone? Don’t miss a MacroEdge beat with all of our Macro Notes, research, data, discussions and more:

Key Macro Data This Week

With federal government layoffs underway and employment softening continuing, the October cut is all but a lock now, priced at almost 99%. The expected government shutdown length is now up to about 30 days, though there is a small chance it opens on the 15/16th if consensus is reached between parties. Given the desire to keep the data in the dark, it’s likely that the Admin is waiting until post-FOMC to come to the negotiating table. It’s a relatively quiet week for macro data given the shutdown, outside of the Powell speech on Tuesday. In the event of a reopening, I will update the calendar to reflect upcoming data releases.

Monday

Columbus Day holiday - bond market & Federal Reserve closed

Tuesday

Fed Chair Powell speaks

Wednesday

n/a

Thursday

7 Fed Speakers

Philadelphia Fed Data

*Retail Sales

Friday

Uchida Speech (JP)

Cheers from the Casino / Holiday Releveraging

The social media / retail crowd was rejoicing this evening on the resumption of ‘TACO’ policy as it pertains to Chinese tariff announcements. Ironically, much of the Friday move occurred before the tariff post on Truth Social, and was much more liquidity / macro risk-off driven, but the result is NQ futures being about 2% higher to start the week:

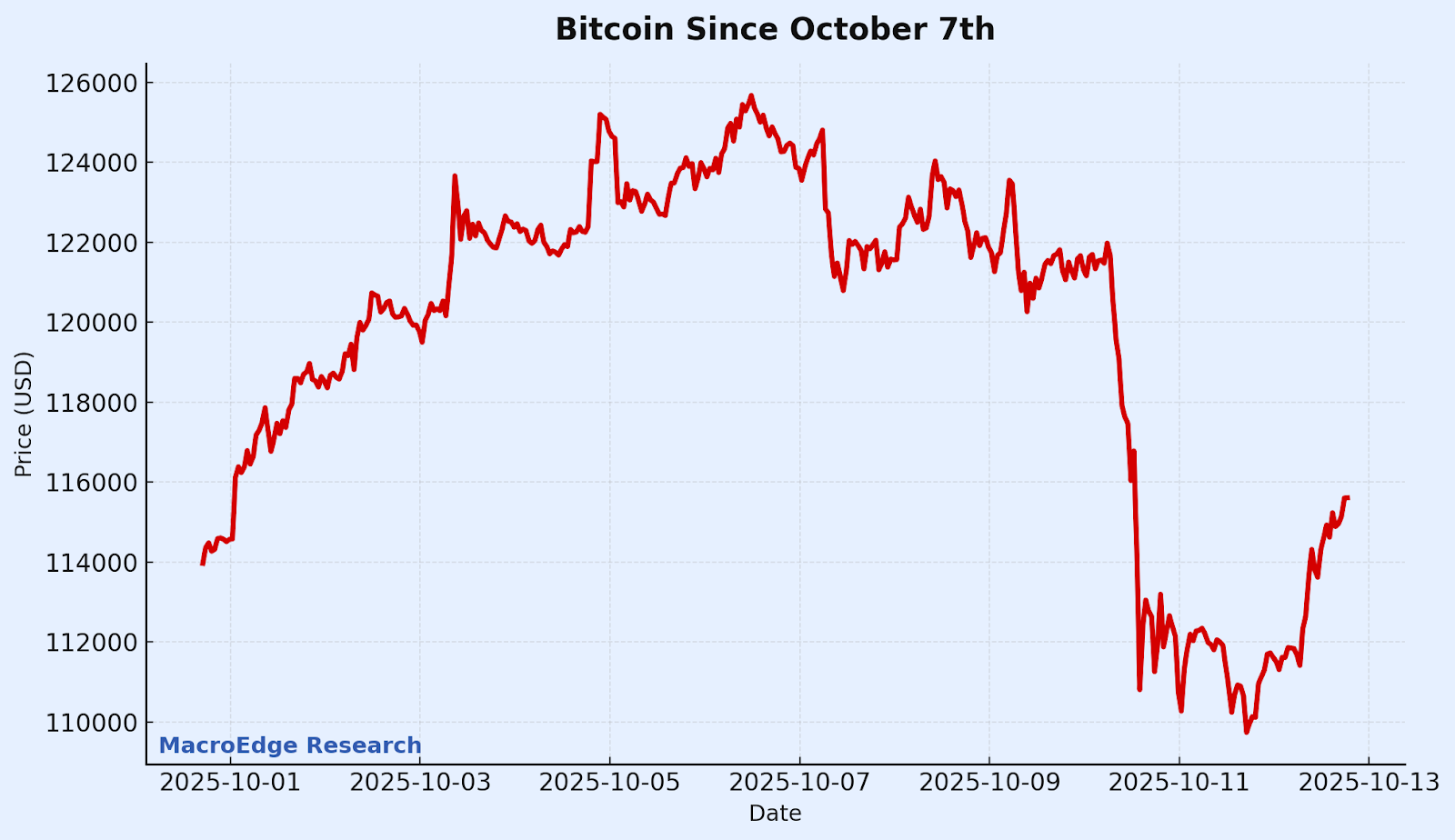

Bitcoin has also retracted about half of the leverage-unwind driven Friday selloff:

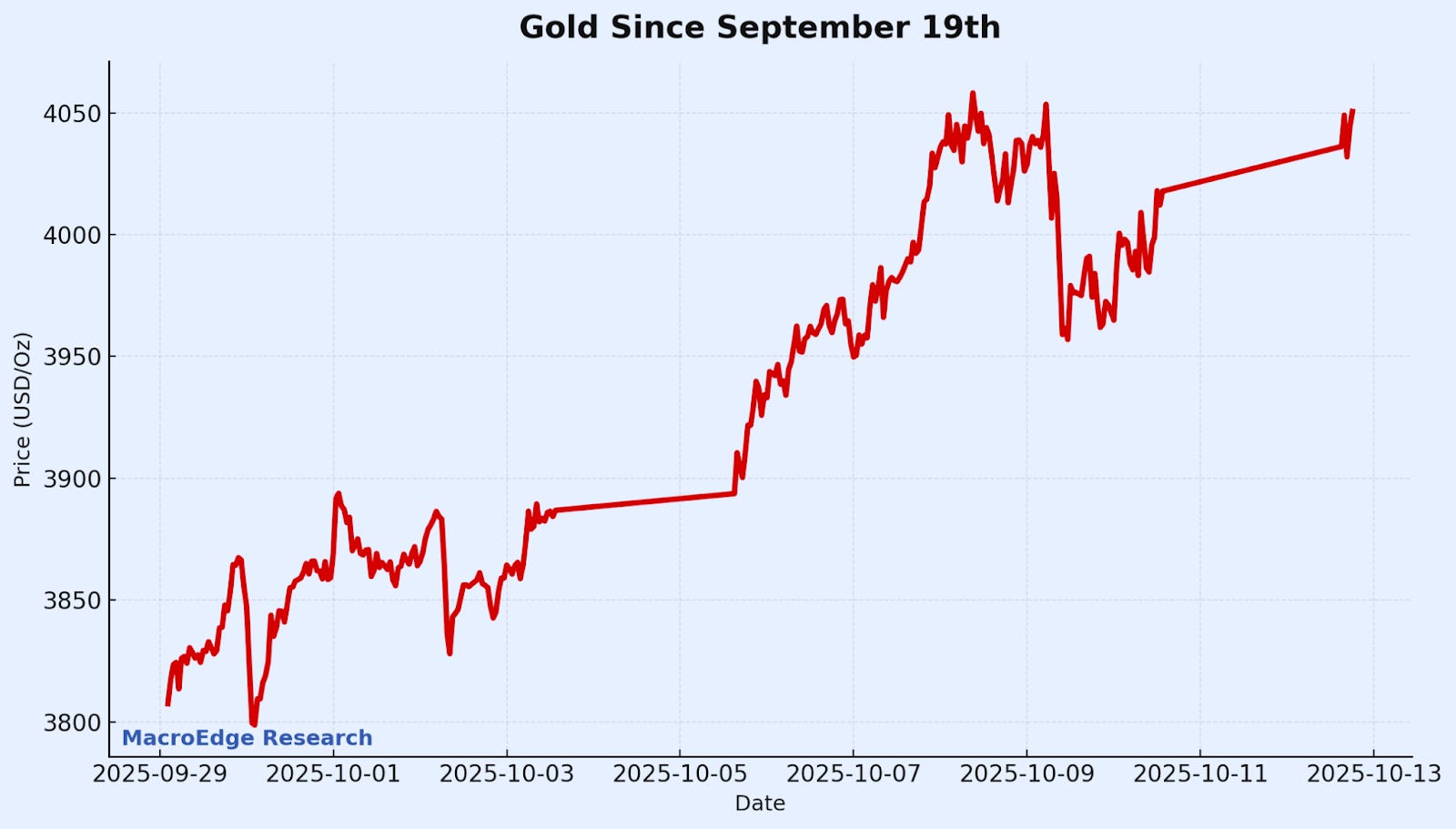

Spot gold - another ATH at $4,060/oz

Monday is noise, and US investors should wait until Friday to determine the broader impact of the Friday deleveraging, if any impact at all, as we head into another macro-weakness driven rate cut. Markets in Asia aren’t feeling as much positivity, though the Nikkei is up about 1% to start the week.

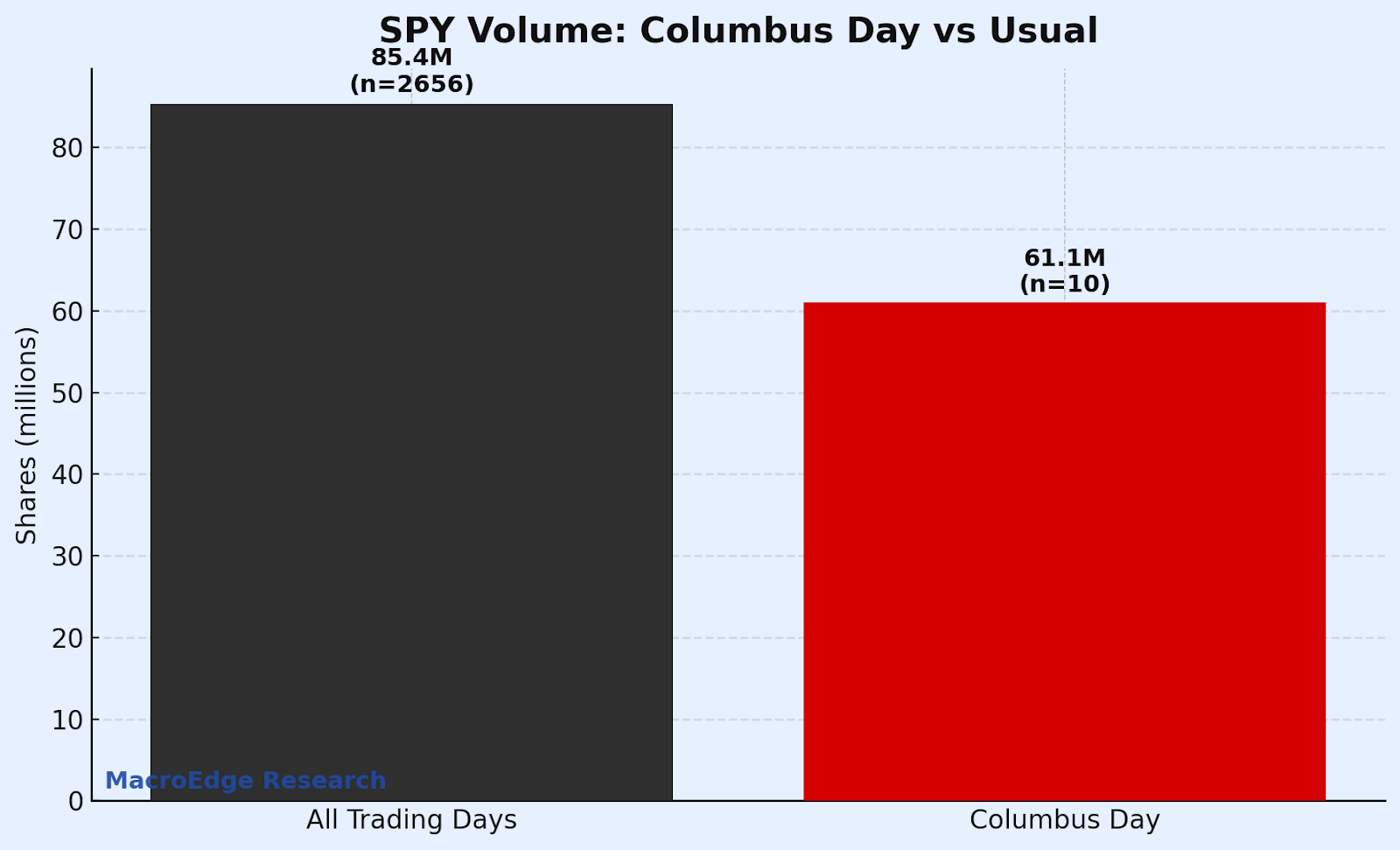

Columbus Day is Usually Quiet

Columbus Day (a bond market & Fed holiday) is usually a quiet trading day, with volume lower than the average trading day.

The MOAB: A Universa Mindset for Q4

The U.S. market today sits at the intersection of leverage, policy intervention, and narrative reflexivity. Like every great bubble, it is built on the illusion of stability born from policy engineering. The government’s fiscal largesse and the Fed’s implicit put have insulated equity valuations from the underlying deterioration in real economic data. This insulation breeds fragility. In Universa’s framework from my broad interpretation, the greater the illusion of permanence, the more convex the eventual resolution. The AI narrative has become the new liquidity conduit, concentrating capital into a handful of assets that now dictate the illusion of broad prosperity. But beneath that surface, credit stress, decelerating earnings breadth, and historically inverted yield curves signal that the convexity engine is already primed. The resolution of such bubbles is never a gentle mean reversion; it’s historically a generational regime change. When the policy impulse fails to generate incremental belief, when liquidity velocity collapses, and when the marginal buyer disappears, the unwind is nonlinear. This bubble will likely resolve through an eventual violent repricing of duration and equity risk, unless we choose a historic second wave of inflation & currency devaluation. The system’s stability is now a function of confidence rather than cash flow, and confidence is the most leveraged asset of all.

The picture outside of AI is one that we should play continuous close attention to as the broader macro picture continues to soften:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.